June 20, 2016

Q1 2016 Share Price Performance (Part 3)

Tier 2 Canadian Healthcare Companies – negative but no panic (same as Tier 1)

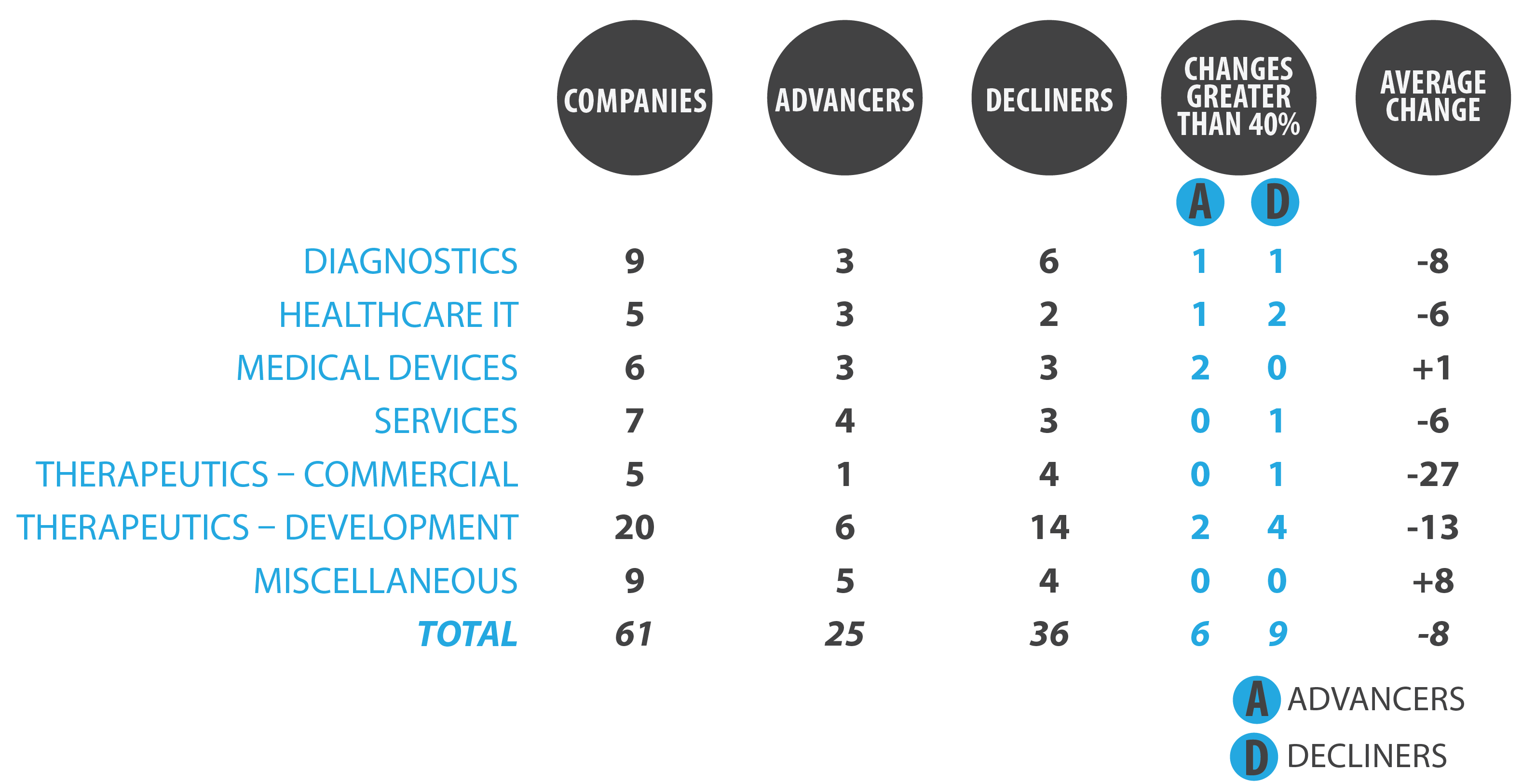

In this blog, I am going to comment on the Q1 2016 share price performance of the group of 61 companies with share prices of between $0.10 and $0.99 to start 2016.

- Decliners outnumbered advancers by 36 to 25 (better than Tier 1)

- Average and median share price changes were -8% and -9%, respectively (slightly better than Tier 1)

- Six companies in this group had share price increases of 40% or more (10% of companies versus 4% in Tier 1)

- Response Biomedical (+75%) – announced Q4 financial results, including a small net profit; share price has returned to H1 2015 trading range

- Critical Outcome Technologies (+71%) – started first clinical trial and completed a small financing

- Arch Biopartners (+56%) – no major news, sporadic and light trading volume

- Vigil Health Solutions (+56%) – announced positive financial results; very sporadic and very light trading volume

- Profound Medical (+44%) – announced a development agreement with Siemens Healthcare and, after the end of the quarter, it received CE Mark approval for the commercial sale of TULSA-PROTM in the EU

- Opsens (+40%) – announced 510(k) clearance from the U.S. FDA for the OptoWire II, a device which is used in diagnosis of the severity of coronary stenosis

- Nine companies had a share price decline of more than 40% (15% of companies in both Tier 1 and 2)

- ImmunoVaccine (-41%) – no negative product news but probably financial concerns; share price recovered most of the Q1 loss in the first couple weeks of April

- Smart Employee Benefits (-50%) – no negative corporate news during the quarter; the Q1 decline was a continuation from prior quarters but the share price bounced to start Q2

- QuikFlo Health (-54%) – share price gains in December 2015 were lost in Q1; no major negative news

- Patient Home Monitoring (-58%) – the share price appeared to have stabilized in Q4 but it declined slowly in Q1, perhaps reflecting the general market movement and some concerns about service pricing

- DiagnoCure (-58%) – an asset sale in Q1 was followed in April by the decision to liquidate and dissolve the company

- Avapecia Life Sciences (-67%) – very sporadic and very light trading volume and value

- Network Life Sciences (-74%) – no news; sporadic and light trading

- Revive Therapeutics (-77%) – no major news; sporadic and light trading

- Telesta Therapeutics (-84%) – announced that the U.S. FDA issued a Complete Response Letter to Telesta’s BLA for MCNA, indicating that an additional Phase 3 clinical trial would be necessary

Medical Marijuana Group

Fourteen public Canadian medical marijuana companies are being monitored for share price performance in 2016. Most companies in this sector are in the early stages of commercialization, either still seeking Health Canada licenses or not yet profitable.

- There were 5 advancers and 9 decliners in Q1

- Average and median share price changes were -3% and -16%, respectively

- Two companies (tickers VRT, BLO) had share price increase of 40% or more while three companies (tickers MJN, BCC, VP) had share price decreases of 40% or more

Looking Ahead

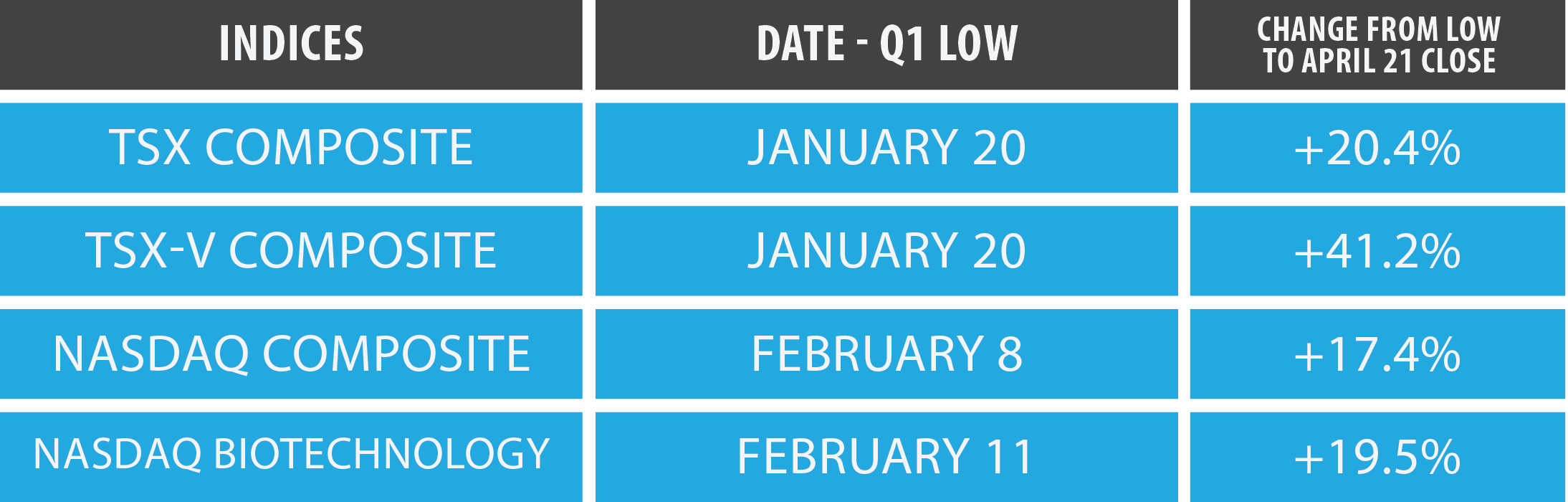

All major indices have bounced off their Q1 lows, as illustrated in the table below. The major surprise is the strength of the bounce for the TSX Venture Composite Index, which means that junior mining stocks are hot again. This could result in a mixed outlook for Canadian junior healthcare stocks – risk capital is coming back into the market but will it be company and sector selective or adopt the herd mentality and simply buy the junior mining sector.

- Will the sector be impacted again by the U.S. elections? If the polls say something is to be gained, I am sure the subject will be raised again. However, with the two major targets, Valeant’s Pearson and Turing’s Shkreli, leaving the sector, the tone of any comments will probably be muted compared to the impact in Q3 2015.

- Will the new U.S. tax inversion guidelines impact the sector? It obviously terminated the Pfizer-Allergan merger and may preclude a few other deals in the short term. The new guidelines just mean that any tax inversion strategy will have to be planned over several years. Head offices will move when there is a net advantage from tax and other perspectives.

[The author and his immediate family members may have long or short positions in the shares of some companies mentioned in or assessed during the preparation of this blog. Past share price performance may not be an indicator of future share price performance. This blog does not consider the investment objectives, financial situation or particular needs of any particular person. Investors should obtain professional advice based on their own individual circumstances before making an investment decision.]

As with all our posts, please see our full legal disclaimer