May 8, 2023

Q1 2023 Share Price Performance

Healthcare Stocks Continue Their Modest Rebound

In this blog post, Bloom Burton’s equity research team summarizes the performance of the Canadian healthcare sector during 1Q-2023 and provides commentary on select stock movements and overall market trends.

Inclusion Criteria

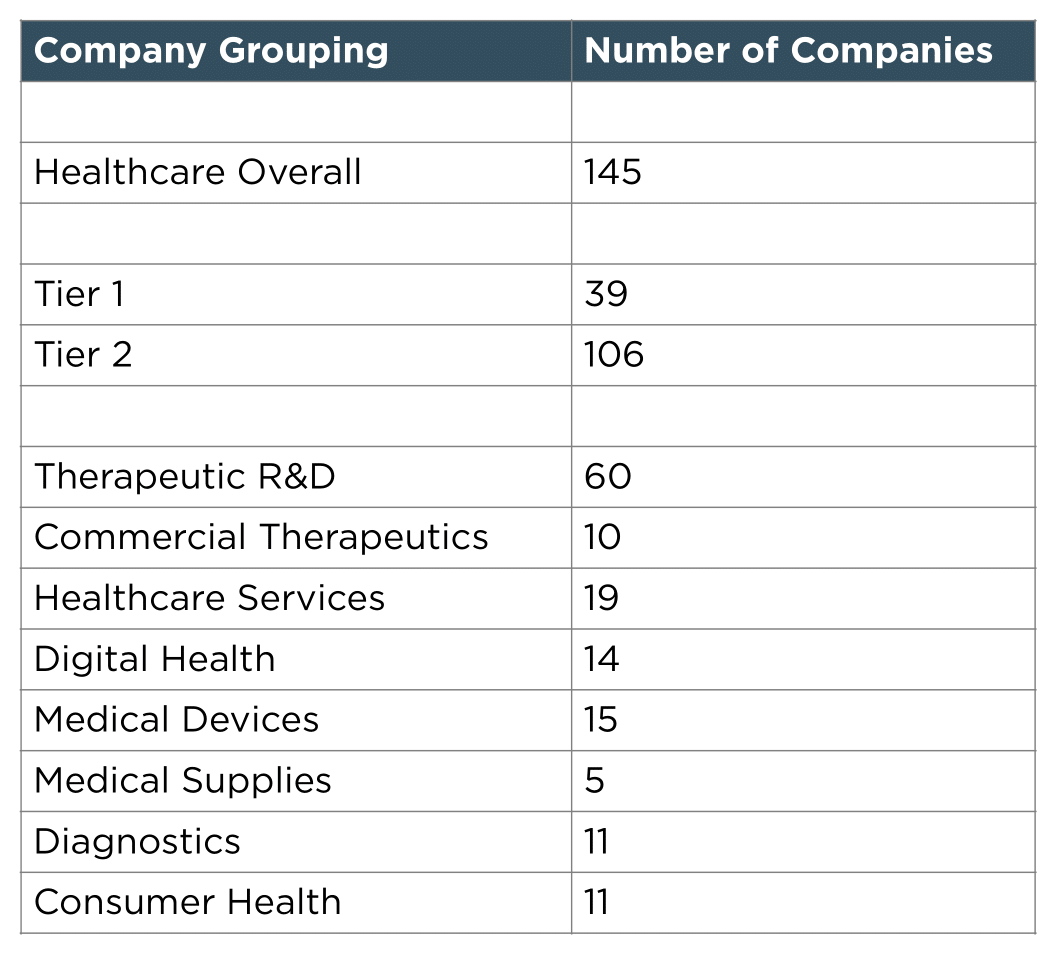

The analysis includes all Canadian publicly listed healthcare companies, defined as companies that are Canadian headquartered and/or listed on Canadian exchanges, with either a market cap (MC) or enterprise value (EV) of C$10M or greater at March 31. Our definition of healthcare includes companies operating in the following areas: therapeutic R&D; commercial therapeutics; healthcare services; digital health; medical devices; medical supplies; diagnostics; and consumer health. We do not include medical cannabis or psychedelic medicine companies (unless they are developing cannabis or psychedelic-based products under the traditional drug development regulatory process) or companies that operate long-term care facilities. Based on these criteria we identified 145 companies.

We classify companies as “Tier 1” and “Tier 2” based on their MC – Tier 1 companies are those with MC of >C$100M and Tier 2 are those with MC of <C$100M (for a complete listing of companies included in Tiers 1 and 2 of Bloom Burton’s “blog universe”, please see Appendix 1 at the end of the blog).

1Q-2023 Performance

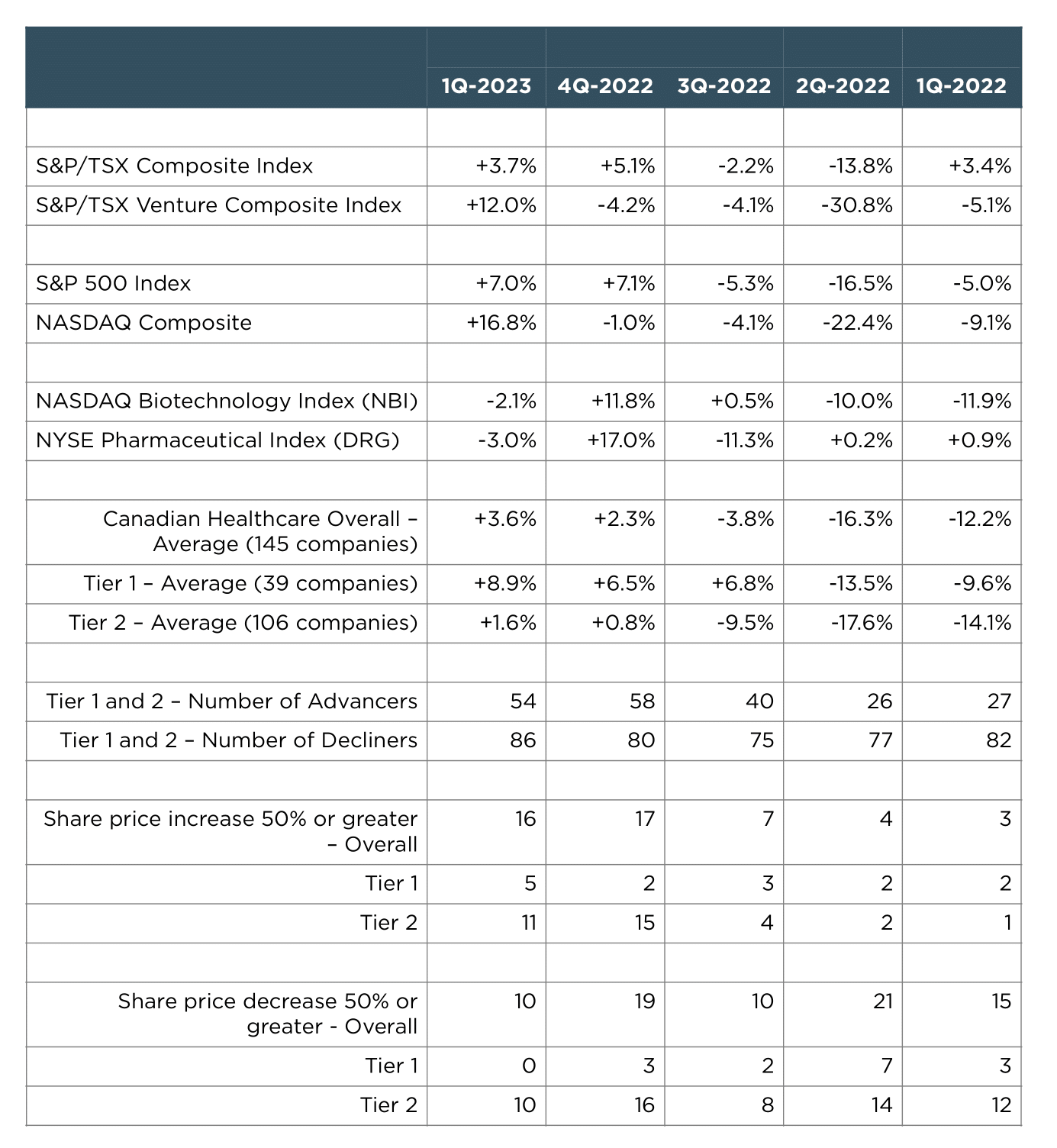

As a group, the 145 Canadian healthcare companies included in Bloom Burton’s 1Q-2023 blog universe were up an average 3.6% in the quarter, performing in line with the S&P/TSX Composite Index (+3.7%), but underperforming the S&P/TSX Venture Composite Index (+12.0%). This marks the second positive quarterly performance for the group since 3Q-2021, when the sector returned 0.4%.

Following a strong 4Q-2022, U.S. biotech stocks, which normally lead Canadian stocks, were back in negative territory in 1Q-2023 – the NASDAQ Biotechnology Index (NBI) lost 2.1% in 1Q-2023, underperforming the broader U.S. market (S&P 500 Index was up 7.0%; NASDAQ Composite was up 16.8%). We believe the modest underperformance of U.S. biotech stocks vs their Canadian peers was due to a pull back following their strong outperformance the previous two quarters, reflecting a reversion to the mean. Following the sector’s dismal performance since 3Q-2021, resulting from a general risk-off investment environment and concerns about drug pricing regulation, we appear to be reaching a bottom. However, with low valuations and the large balance sheets of big pharma, we are primed for an M&A-fueled sector rally.

The NYSE Pharmaceutical Index (DRG), which consists of large, well-capitalized, pharma companies, had a similarly weak performance this quarter (down 3.0% vs the NBI’s 2.1% loss), following a very strong performance in 4Q-2022 (was up +17.0%).

Among Canadian healthcare companies, larger Tier 1 companies, which are typically better capitalized and less risky, performed better than smaller Tier 2 companies in 1Q-2023 (+8.9% vs +1.6%, respectively).

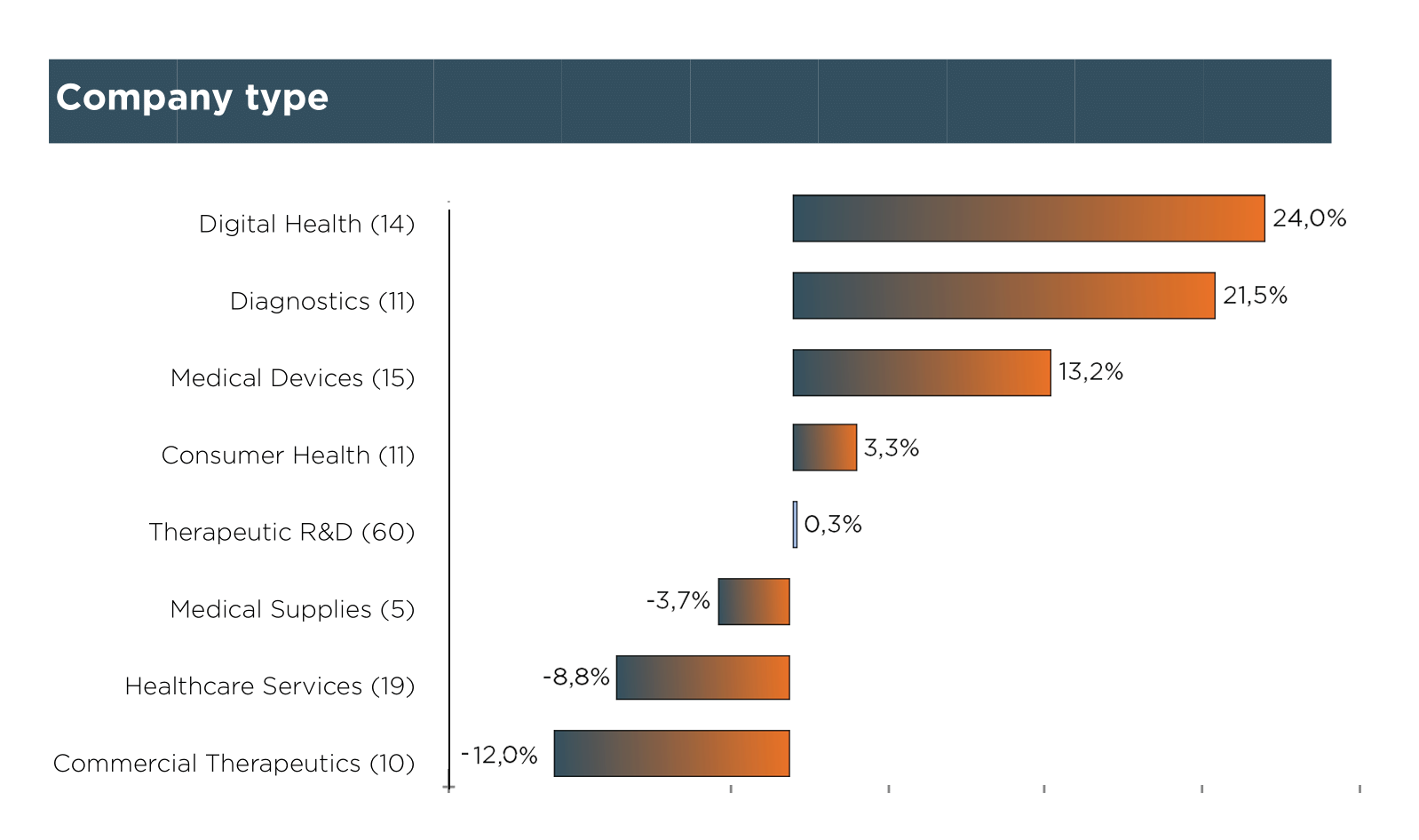

Among the healthcare subsectors in Bloom Burton’s Canadian tracking universe, the best performing subsectors were digital health (14 companies: +24.0%), diagnostics (11 companies: +21.5%) and medical devices (15 companies: +13.2%), which were each boosted by a few high performing names (NetraMark Holdings Inc.: +147.5%; Predictmedix Inc.: +187.5%; Neovasc Inc.: +96.0%; NuGen Medical Devices Inc.: +353.5%). Other sectors had more of a mixed bag of performances, including consumer health (11 companies: +3.3%), therapeutic R&D (60 companies: +0.3%), medical supplies (5 companies: -3.7%), healthcare services (19 companies: -8.8%) and commercial therapeutics (10 companies: -12.0%).

1Q-2023 Healthcare Stock Performance By Subsector:

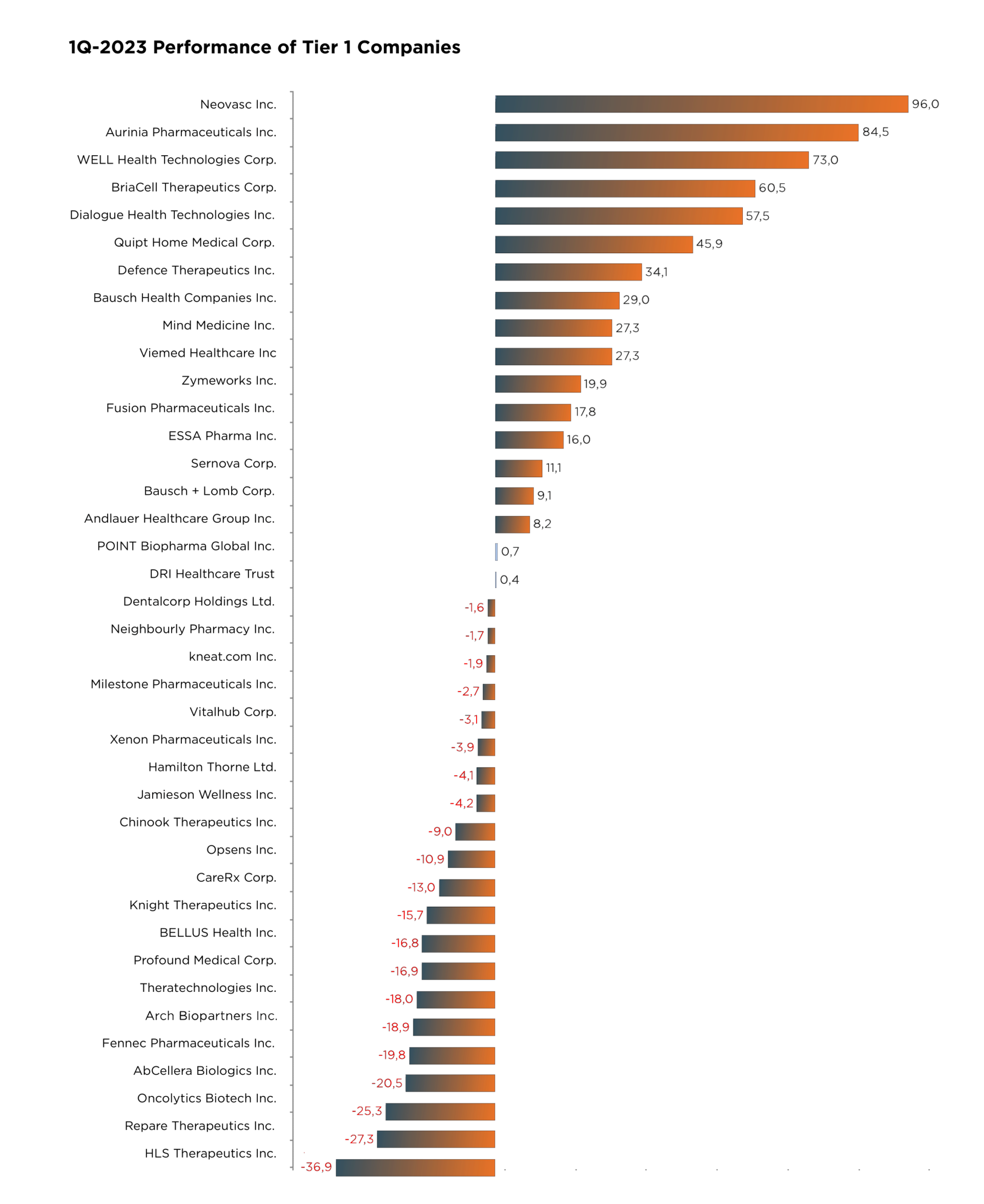

Tier 1 Company Performance

Overall, we included 39 companies in our Tier 1 analysis with MC of $100M or greater, which collectively had a 1Q-2023 return of 8.9%.

The number of Tier 1 advancers (18) was just below the number of decliners (21) this quarter.

Notable Tier 1 advancers in the quarter were:

- Neovasc Inc. – The stock gained 96.0% during 1Q-2023 following the announcement that it had an agreement to be acquired by Shockwave Medical.

- Aurinia Pharmaceuticals Inc. – AUPH was up 84.5% in the quarter after the company reported 4Q-2022 financial results and PTAB terminated the Inter Partes Review of one its patents and reported 1Q-2023.

- WELL Health Technologies Corp. – The stock appreciated 73.0% in the quarter after the company reported 4Q-2022 financial results and made an investment in doctorly GmbH.

- BriaCell Therapeutics Corp. – The stock gained 60.5% in 1Q-2023, after it provided an update on its end of phase 2 meeting with the FDA for Bria-IMT combination in advanced metastatic breast cancer.

- Dialogue Health Technologies Inc. – The stock was up 57.5% in the quarter following a business update and reported 4Q-2022 financial results.

There were no Tier 1 companies with share price declines ≥50% this quarter.

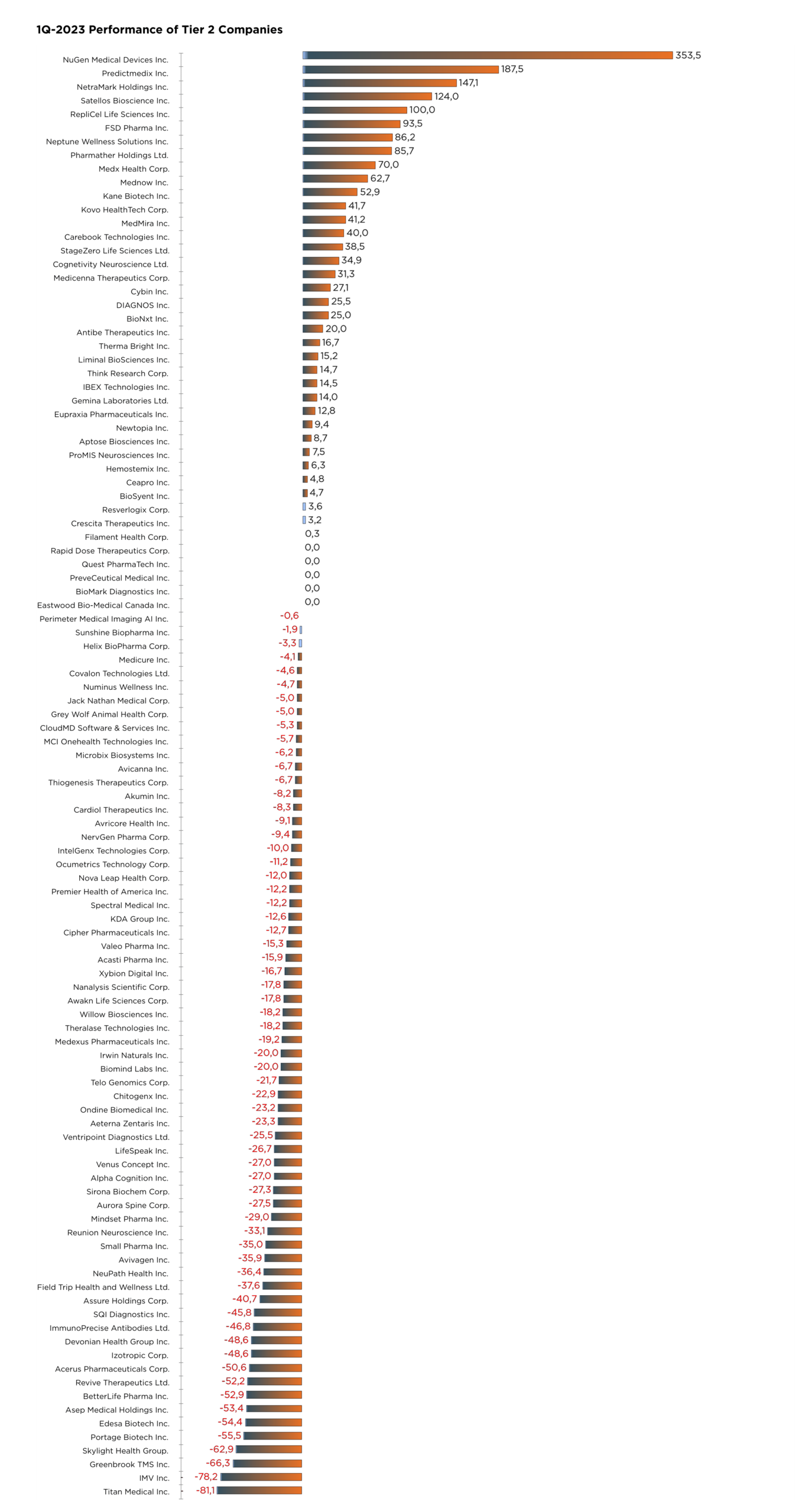

Tier 2 Company Performance

Overall, we included 106 companies in our Tier 2 analysis (with MC of less than $100M), which as a group had a 1Q-2023 return of 1.6%.

The number of advancers (36) was lower than the number of decliners (65).

Notable advancers in the quarter include:

- NuGen Medical Devices Inc. – The stock was up 353.5% in the quarter, after the company announced a series of management and board appointments, as well as efficacy results for its needle-free insulin injection device in patients with diabetes.

- Predictmedix Inc. – The stock appreciated 187.5% in 1Q-2023, after the company announced upcoming milestones and provided a commercialization outlook, announced a $0.6M private placement, as well as several other corporate updates.

- NetraMark Holdings Inc. – The stock climbed 147.1%, after the company announced a business change to focus on pharmaceutical AI.

- Satellos Bioscience Inc. – The stock rose 124.0% in the quarter following the reporting of preclinical data in a muscular dystrophy disease model and announced progress with a development candidate.

- RepliCel Life Sciences Inc. – The stock rose 100.0% in 1Q-2023, rising steadily since the company announce a corporate update late last year.

- FSD Pharma Inc. – The stock was up 93.5% in the quarter, after it received regulatory clearance for its proposed phase 1 clinical trial of Lucid-21-302, its multiple sclerosis candidate.

- Neptune Wellness Solutions Inc. – The stock rose 86.2% in the quarter after the company announced the closing of a debt facility.

- Pharmather Holdings Ltd. – The stock climbed 85.7% in 1Q-2023, following an update on Ketarx (racemic ketamine) and expected milestones for 2023.

- Medx Health Corp. – The stock rose 70.0% in the quarter, following the closing of multiple convertible debenture financings.

- Mednow Inc. – The stock was up 62.7% in the quarter, after the closing of the first tranche of a $4M senior secured convertible debenture.

- Kane Biotech Inc. – The stock climbed 52.9% in the quarter, following the extension of its credit term facility.

Notable decliners in the quarter include:

- Titan Medical Inc. – The stock was down 81.1% in the quarter, after the company announced that it has halted development of Enos among other cost-cutting measures.

- IMV Inc. – The stock declined 78.2% in 1Q-2023, following the reporting of initial results from the MVP-S phase 2b VITALIZE trial.

- Greenbrook TMS Inc. – The stock declined 66.3% in the quarter, after the company drew down an additional US$3M in debt financing and announced a restructuring plan to reduce costs, streamline operations and achieve profitability.

- Skylight Health Group Inc. – The stock was down 62.9% in 1Q-2023, after the company announced a closure of operations in Colorado.

- Portage Biotech Inc. – The stock fell 55.5% in the quarter, after the company reported 4Q-2022 financial results.

- Edesa Biotech Inc. – The stock declined 54.4% in the quarter, after the company reported topline phase 2b data for its dermatology drug, EB01 for allergic contact dermatitis.

- Asep Medical Holdings Inc. – The stock was down 53.4% in 1Q-2023, after the company signed letters of intent with Bahrain and China-based partners to commercialize its sepsis diagnosis technology.

- BetterLife Pharma Inc. – The stock lost 52.9% in the quarter, after the company announced a $1.9M public offering.

- Revive Therapeutics Ltd. – The stock lost 52.2% in 1Q-2023, following an update on the company’s update on a phase 3 clinical trial for bucillamine in COVID-19.

- Acerus Pharmaceuticals Corp. – The stock fell by 50.6% in 1Q-2023, after the company filed for CCAA protection.

Click Here to View the Appendix

Disclaimer:

Information included in this blog post has been sourced from publicly available sources. No representation or warranty, express or implied, is made with respect to the accuracy, correctness or completeness of the information contained herein. The commentary in this blog post represents the views and opinions of Bloom Burton only and should not be relied upon as investment advice. Bloom Burton accepts no liability whatsoever for any direct or consequential loss arising from any use or reliance on the information contained herein. The blog is published on a quarterly basis.