July 13, 2023

Q2 2023 Share Price Performance

Small Cap Healthcare Stocks Lag Behind their Larger Cap Peers and the Broader Markets

In this blog post, Bloom Burton’s equity research team summarizes the performance of the Canadian healthcare sector during 2Q-2023 and provides commentary on select stock movements and overall market trends.

Inclusion Criteria

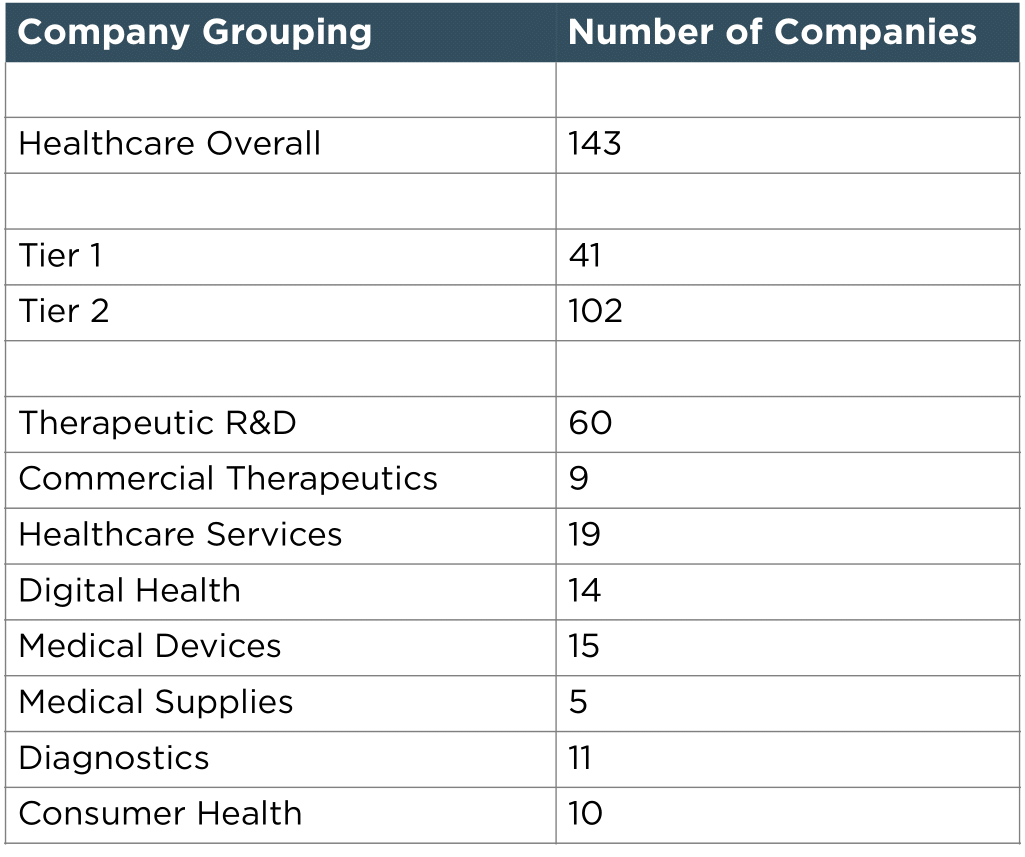

The analysis includes all Canadian publicly listed healthcare companies, defined as companies that are Canadian headquartered and/or listed on Canadian exchanges, with either a market cap (MC) or enterprise value (EV) of C$10M or greater at June 30 (or were acquired for greater than that amount during the quarter). Our definition of healthcare includes companies operating in the following areas: therapeutic R&D; commercial therapeutics; healthcare services; digital health; medical devices; medical supplies; diagnostics; and consumer health. We do not include medical cannabis or psychedelic medicine companies (unless they are developing cannabis or psychedelic-based products under the traditional drug development regulatory process) or companies that operate long-term care facilities. Based on these criteria we identified 143 companies.

We classify companies as “Tier 1” and “Tier 2” based on their MC – Tier 1 companies are those with MC of >C$100M and Tier 2 are those with MC of <C$100M (for a complete listing of companies included in Tiers 1 and 2 of Bloom Burton’s “blog universe”, please see Appendix 1 at the end of the blog).

2Q-2023 Performance

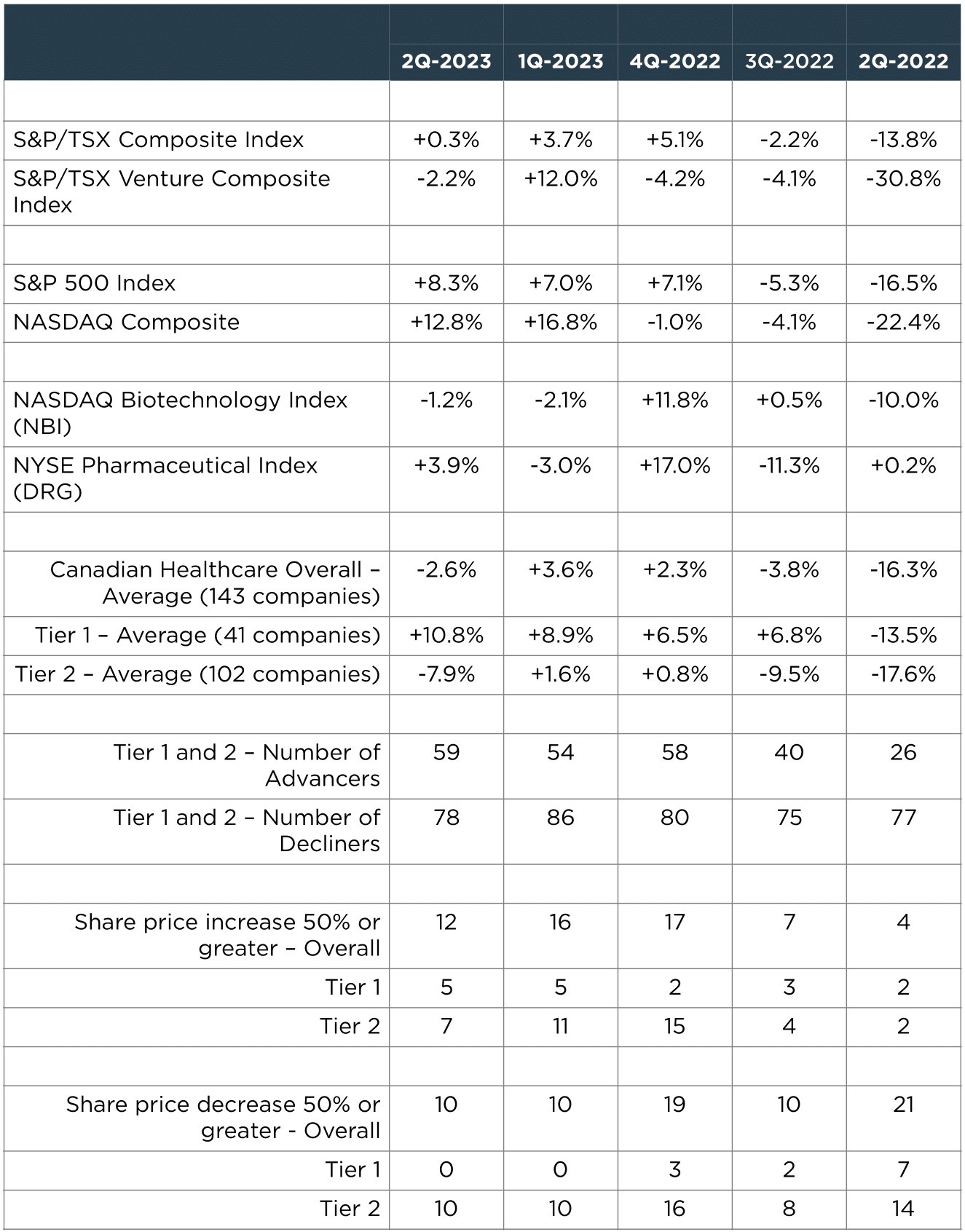

As a group, the 143 Canadian healthcare companies included in Bloom Burton’s 2Q-2023 blog universe were down an average 2.6% in the quarter, underperforming the S&P/TSX Composite Index (+0.3%), but in line with the S&P/TSX Venture Composite Index (-2.2%). This marks a return to negative territory for the group, after two consecutive positive quarters.

U.S. biotech stocks, which normally lead Canadian stocks, had a similarly weak performance in 2Q-2023 – the NASDAQ Biotechnology Index (NBI) lost 1.2% in the quarter, underperforming the broader U.S. market (S&P 500 Index was up 8.3%; NASDAQ Composite was up 12.8%). However, the market cap-weighted S&P 500 and the tech-focused NASDAQ indices were heavily skewed by the very strong performance of a handful of AI-focused large tech companies (the equally weighted Dow Jones index was up a more modest 4.7%). The biotech sector in particular, continues to be weighed down by the dismal financing environment, with many smaller companies trading with negative EVs, due to the general risk-off sentiment and as investors have been digesting the impacts of the Inflation Reduction Act (IRA) on drug pricing. M&A activity has been a bright spot, with the most attractive companies being those with validated late-stage assets, and which are typically well capitalized. Greater scrutiny from the Federal Trade Commission (FTC) on pharma mergers is another overhang on the sector, but it does not appear to have negatively impacted M&A to date, although this could change if the FTC successfully blocks Amgen’s acquisition of Horizon.

The NYSE Pharmaceutical Index (DRG), which consists of large, well-capitalized, pharma companies, performed better in 2Q-2023 (up 3.9% vs the NBI’s 1.2% loss), despite lingering concerns over the IRA and FTC.

Among Canadian healthcare companies, there was again a divergence in the performance of the group, with larger Tier 1 companies, which are typically better capitalized and less risky, performing significantly better than smaller Tier 2 companies in 2Q-2023 (+10.8% vs -7.9%, respectively), consistent with the trend seen in previous quarters.

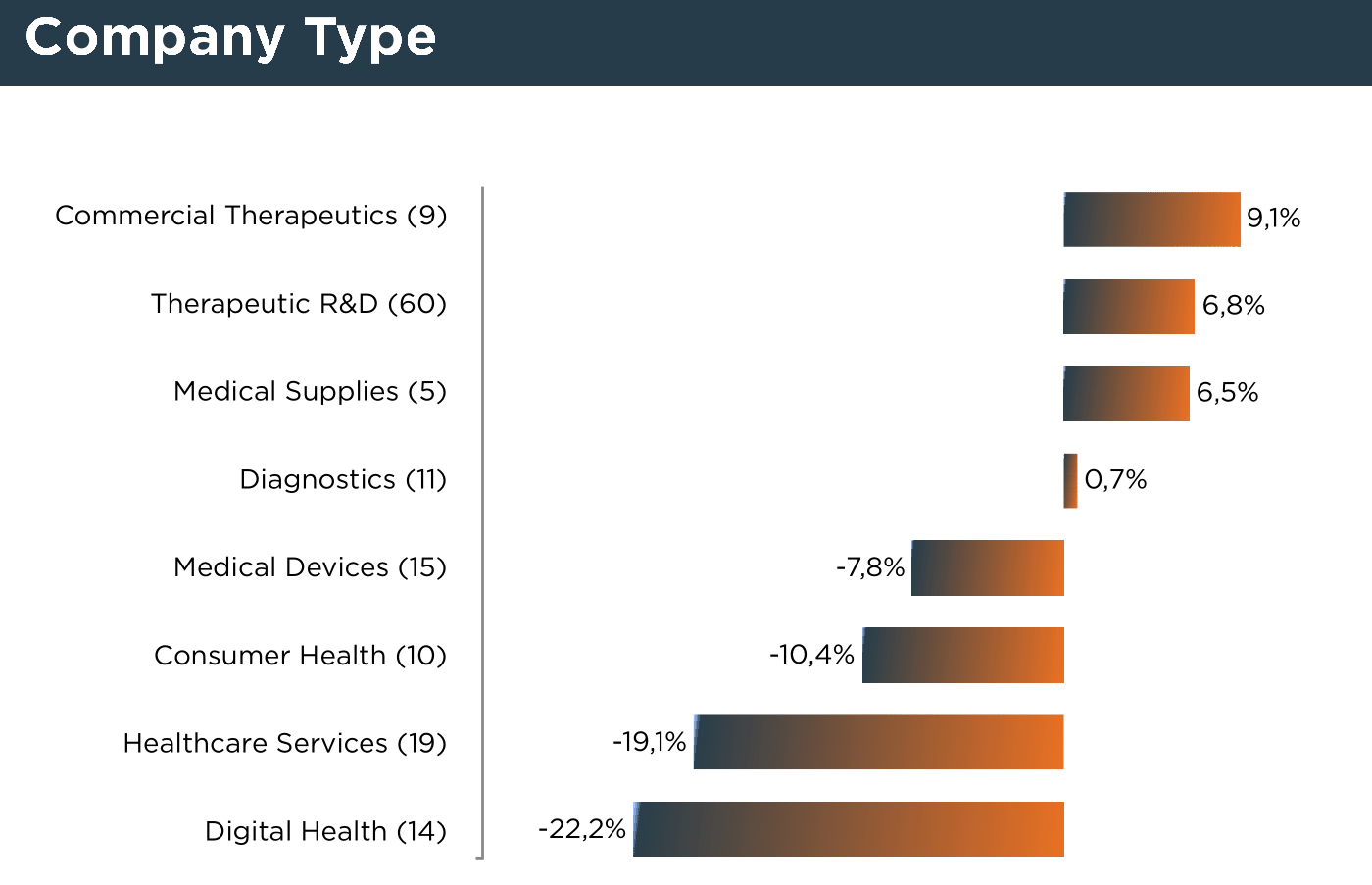

Among the healthcare subsectors in Bloom Burton’s Canadian tracking universe, the best performing subsectors were: commercial therapeutics (9 companies: +9.1%), which was boosted by the strong performance of DRI Healthcare Trust (+53.4%), followed by therapeutics R&D (60 companies: +6.8%), which also benefitted from several takeouts (BELLUS +96.8%; Chinook +96.8%) and clinical readouts (Oncolytics +114.1%; Eupraxia +108.4%), as well as medical supplies (5 companies: +6.5%). All other subsectors had a negative return this quarter, including medical devices (15 companies: -7.8%), consumer health (10 companies: -10.4%), healthcare services (19 companies: -19.1%) and digital health (14 companies: -22.2%).

2Q-2023 Healthcare Stock Performance By Subsector:

Tier 1 Company Performance

Overall, we included 41 companies in our Tier 1 analysis with MC of $100M or greater, which collectively had a 2Q-2023 return of 10.8%.

The number of Tier 1 advancers (22) was higher than the number of decliners (17) this quarter.

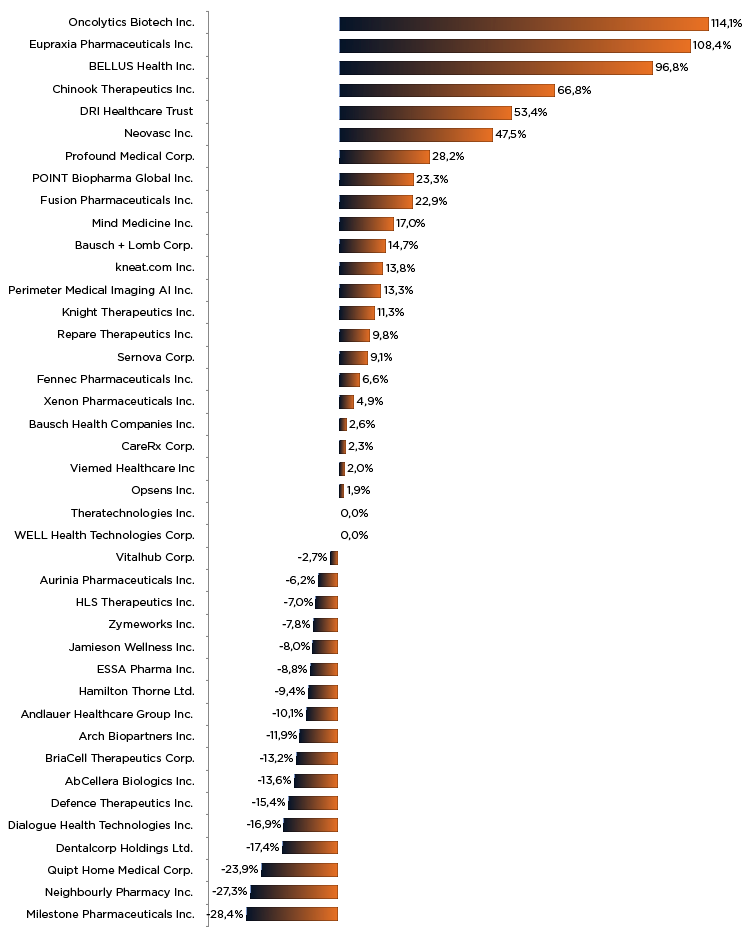

Notable Tier 1 advancers in the quarter were:

- Oncolytics Biotech Inc. – The stock gained 114.1% during 2Q-2023, following the reporting of phase 2 data for its cancer treatment, oncolytic reovirus pelareorep, in metastatic breast cancer (BRACELET-1 trial) at the American Society of Clinical Oncology meeting.

- Eupraxia Pharmaceuticals Inc. – EPRX was up 108.4% in the quarter, with the rise coming in the leadup to its topline readout for its drug, EP-104IAR, in a phase 2b trial in pain associated with osteoarthritis.

- BELLUS Health Inc. – The stock jumped 96.8% after the company announced it was being acquired by GSK for US$2.0B (the deal closed on June 28, 2023).

- Chinook Therapeutics Inc. – The stock gained 66.8% in 2Q-2023 after the company announced that it has entered into an agreement to be acquired by Novartis for US$3.2B, plus a potential $300M in contingent value rights.

- DRI Healthcare Trust – The stock was up 53.4% in the quarter, after the company announced the sale of its TZIELD royalty interest, reported 1Q-2023 financial results and announced the acquisition of a royalty interest in Orserdu.

There were no Tier 1 companies with share price declines ≥50% this quarter.

2Q-2023 Performance of Tier 1 Companies:

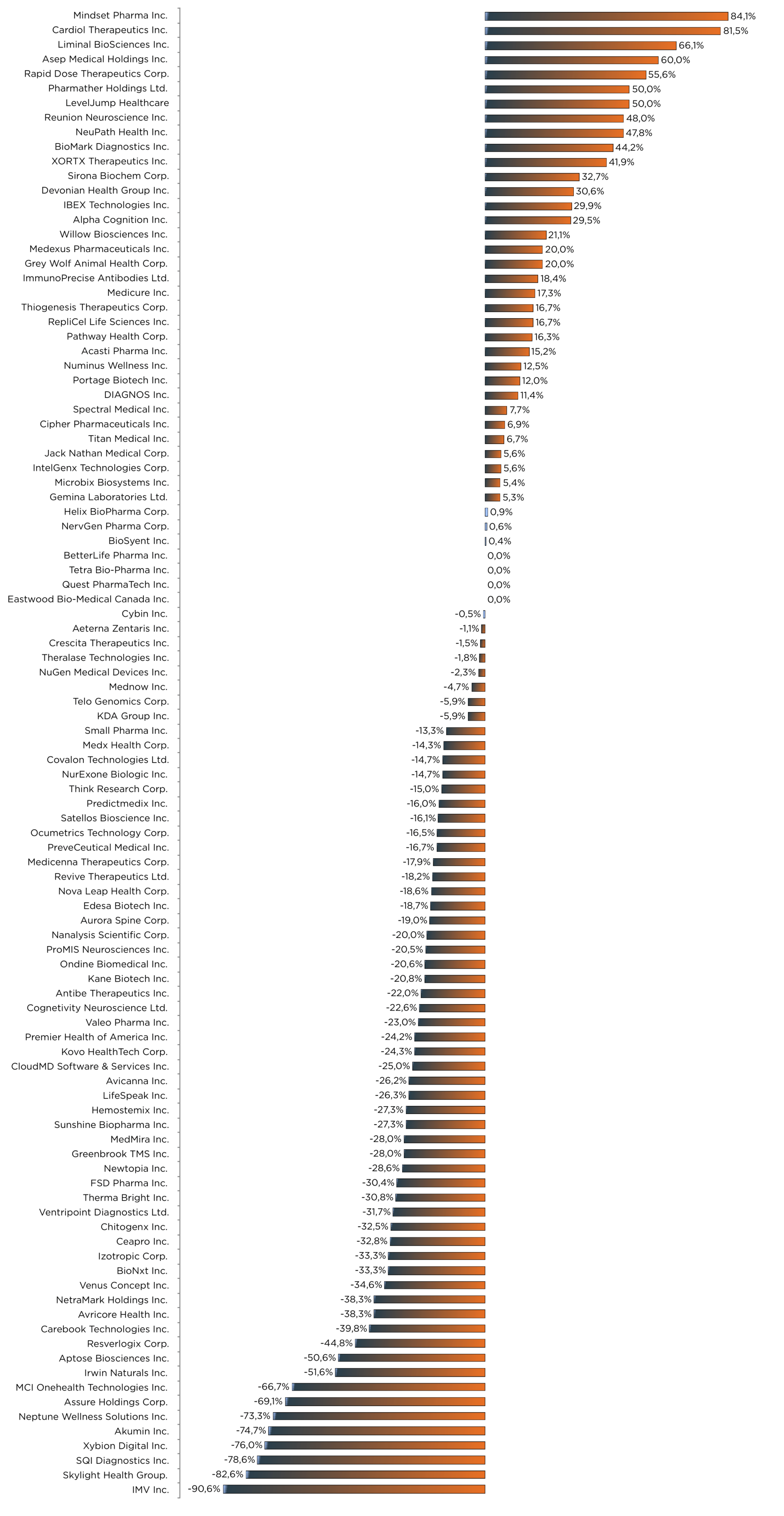

Tier 2 Company Performance

Overall, we included 102 companies in our Tier 2 analysis (with MC of less than $100M), which as a group had a 2Q-2023 return of -7.9%.

The number of advancers (37) was lower than the number of decliners (61).

Notable advancers in the quarter include:

- Mindset Pharma Inc. – The stock was up 84.1% in the quarter, after the CEO issued a letter to shareholders discussing the company’s expanded drug discovery efforts into novel non-hallucinogenic drugs, and the company filed two patent applications for its non-hallucinogen non-tryptamine compounds.

- Cardiol Therapeutics Inc. – The stock appreciated 81.5% in 2Q-2023, after the company reported 4Q-2022 financial results and provided an operational update.

- Liminal BioSciences Inc. – The stock climbed 66.1%, after the company announced the receipt of an unsolicited non-binding transactional proposal from Structured Alpha LP to acquire the remaining 64% of the company’s outstanding shares (proposal values the company at $31.4M; EV of -$5.7M).

- Asep Medical Holdings Inc. – The stock rose 60.0% in the quarter, as the company announced it was close to listing on NASDAQ, as well as announcing new technologies for the rapid detection of therapies against sepsis and superbugs.

- Rapid Dose Therapeutics Corp. – The stock rose 55.6% in 2Q-2023, after the company’s Cease Trade Order was revoked by the Ontario Securities Commission.

- PharmaTher Holdings Ltd. – The stock jumped 50.0% in the quarter, after the company announced that it had entered into a collaboration agreement for the commercialization of KETARX in the U.S. market.

- LevelJump Healthcare Corp. – The stock rose 50.0% in the quarter, after the company announced record revenues for 1Q-2023.

Notable decliners in the quarter include:

- IMV Inc. – The stock was down 90.6% in the quarter, after the company announced that it had initiated restructuring proceedings under the Companies’ Creditors Arrangement Act.

- Skylight Health Group Inc. – The stock declined 82.6% in 2Q-2023, after the company announced it would not be able to file its 4Q-2022 financial results. The stock has been under a Cease Trade Order since May 8.

- SQI Diagnostics Inc. – The stock declined 78.6% in the quarter, after the company announced proposed insider sales and warrant exercises to fund operations.

- Xybion Digital Inc. – The stock was down 76.0% in 2Q-2023, with the decline starting after the company reported 3Q-2023 financial results.

- Akumin Inc. – The stock fell 74.7% in the quarter, after the company announced 1Q-2023 financial results.

- Neptune Wellness Solutions Inc. – The stock declined 73.3% in the quarter, after the company announced an agreement to acquire the remaining ownership interest of an organic baby food brand, secured a $7.5M inventory financing to complete the acquisition and announced a US$4M public offering.

- Assure Holdings Corp. – The stock was down 69.1% in 2Q-2023, after a series of updates, including the reporting of 4Q-2022 financial results, providing a corporate update, reporting preliminary 1Q-2023 financial results and closing a $6M public offering.

- MCI Onehealth Technologies Inc. – The stock lost 66.7% in the quarter, following the reporting of 4Q-2022 financial results and announcing a review of strategic alternatives, the reporting of 1Q-2023 financial results, the completion of a $1.5M debt financing and the sale of the company’s Alberta operations to WELL Health for $2M.

- Irwin Naturals Inc. – The stock lost 51.6% in 2Q-2023, after the company announced a delay in filing its 4Q-2022 financial results, the issuance of a Cease Trade Order and the resignation of a director.

- Aptose Biosciences Inc. – The stock was down 50.6% in the quarter, after the reporting of 1Q-2023 financial results, entering into a $25M committed equity facility and providing a clinical update on its oral kinase inhibitors for hematological malignancies.

2Q-2023 Performance of Tier 2 Companies:

Click Here to View the Appendix

Disclaimer:

Information included in this blog post has been sourced from publicly available sources. No representation or warranty, express or implied, is made with respect to the accuracy, correctness or completeness of the information contained herein. The commentary in this blog post represents the views and opinions of Bloom Burton only and should not be relied upon as investment advice. Bloom Burton accepts no liability whatsoever for any direct or consequential loss arising from any use or reliance on the information contained herein. The blog is published on a quarterly basis.