July 6, 2017

Q2 Share Price Performance in 2017 - Part 1

Overall, Q2 2017 share price performance in the sector was mixed with high volatility.

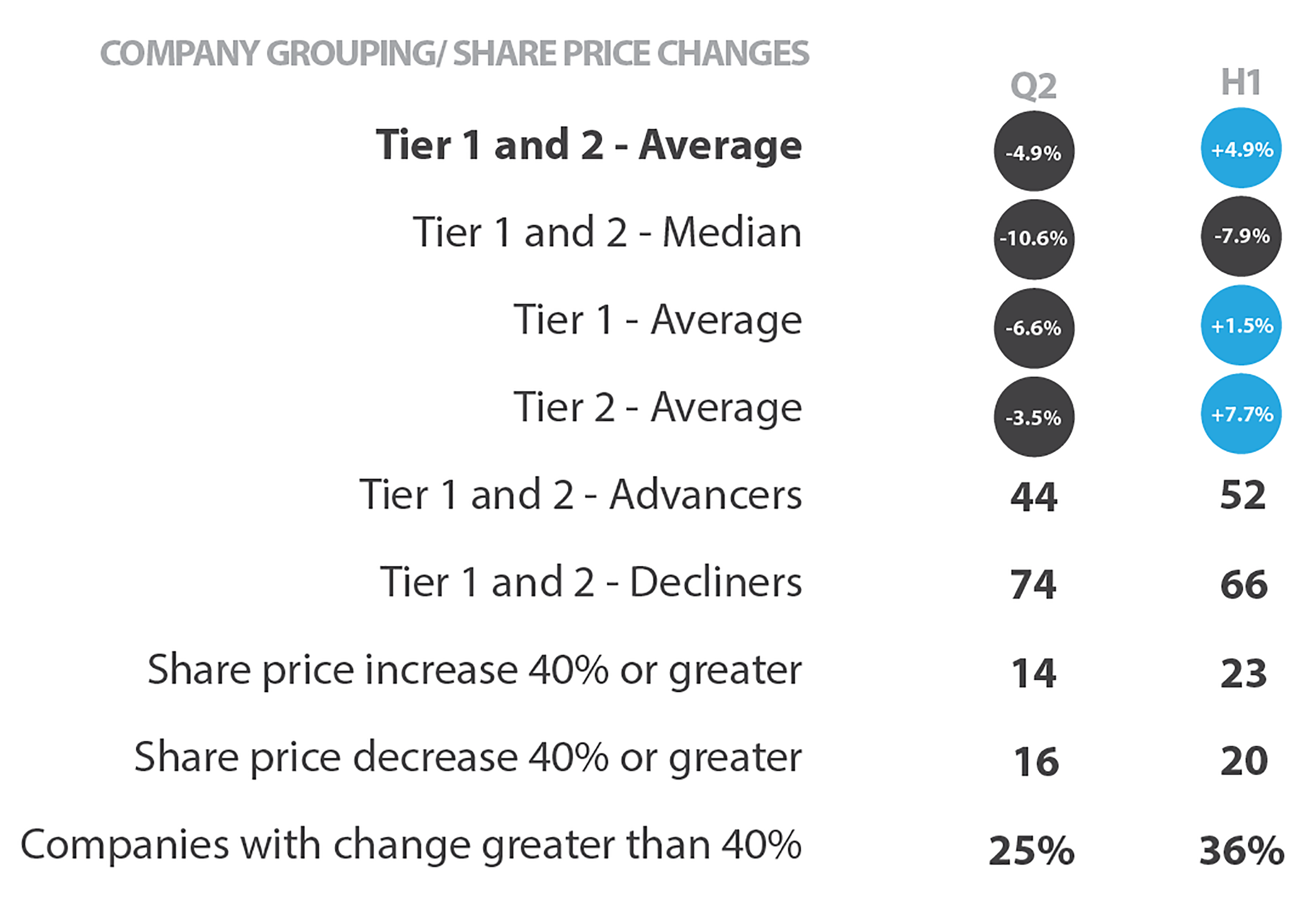

A top-line look at the combined Tier 1 and 2 share price changes shows that despite a poor Q2 (-4.9%), the first half was still positive (+4.9%).

However, a topline look always needs to be followed by a detailed analysis.

The median change in both Q2 and H1 was negative, indicating that a few large positive changes were skewing the averages. Eight companies had their share prices more than double in H1. For most of my personal biotech investing, I look for potential doubles in the next 12 months – it is always nice to see that there are opportunities for those returns. The reasons for these big moves will be outlined in this Q2 blog series.

- Decliners outnumbered advancers, especially in Q2.

- Performance was better for the Tier 2 companies.

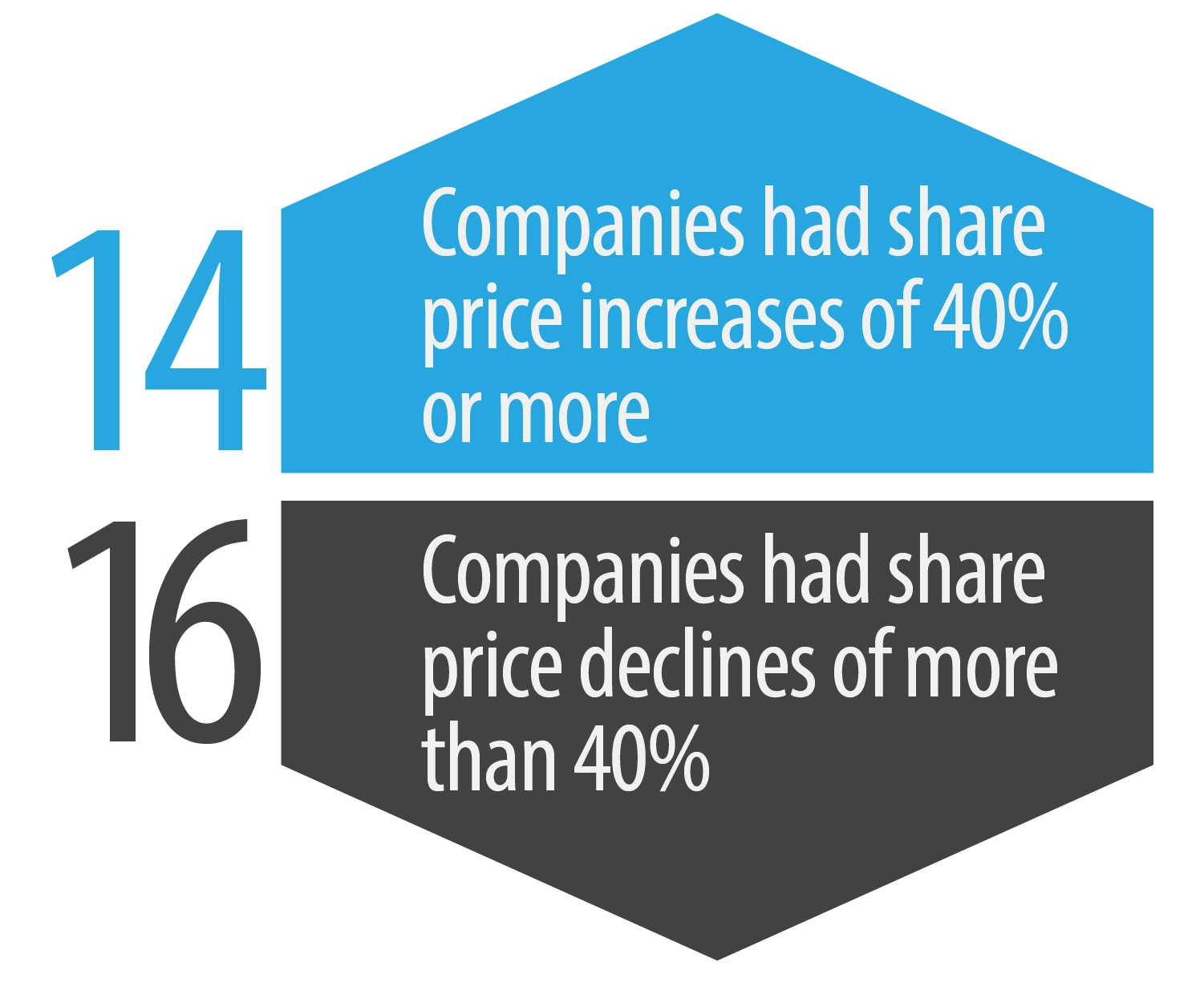

- The sector volatility is high when 36% of the companies have share price changes greater than 40% in H1.

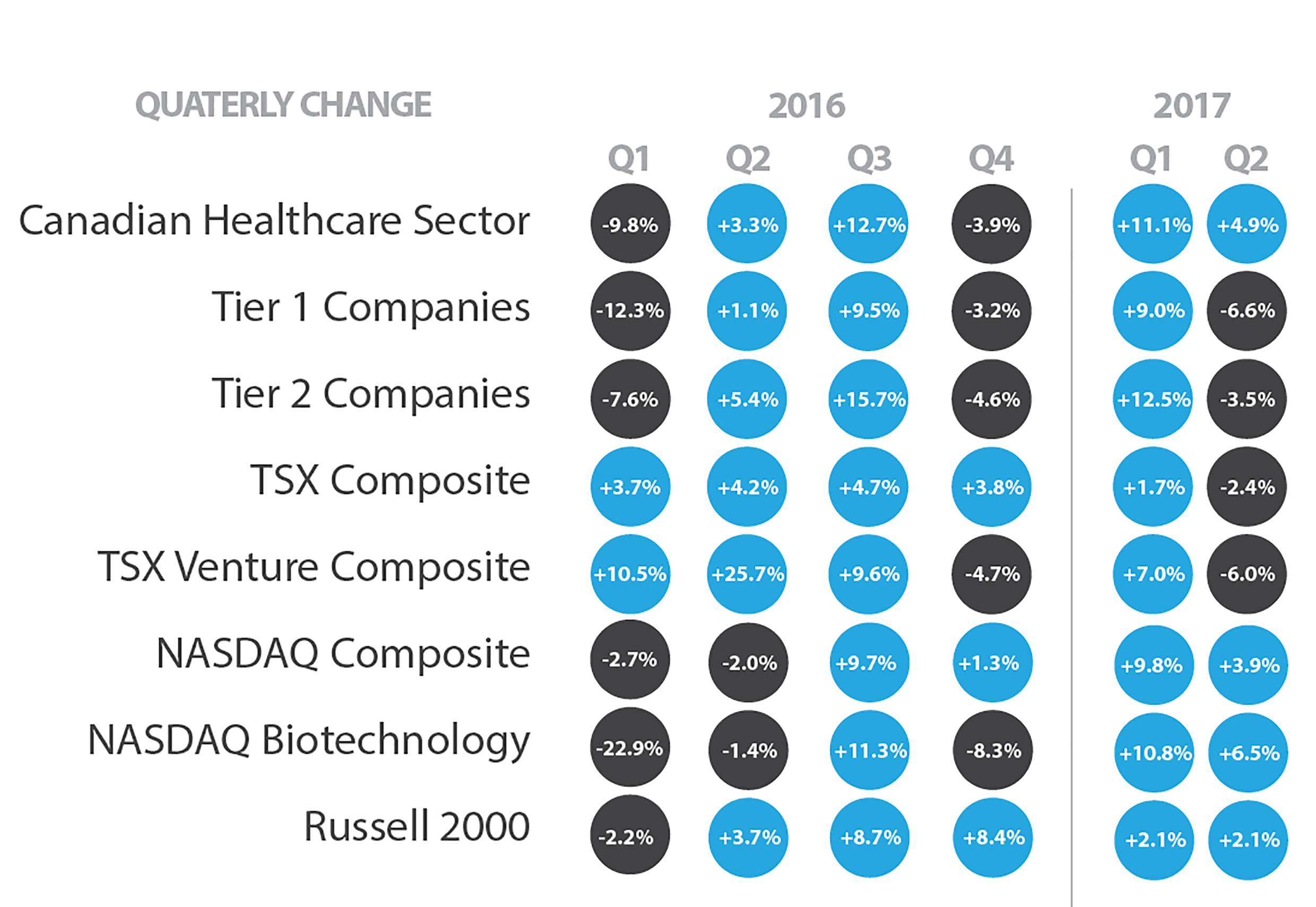

An investor should always ask ‘how does the average share price change compare with some benchmarks in Q2?’ In this share price analysis I included an additional benchmark, the Russell 2000. This benchmark indicates the performance of U.S. small cap stocks.

U.S. markets will sometimes drag the Canadian indices along for the ride, up or down. In the last few months, the U.S. market has been buoyed by some uniquely American factors – the ‘Trump effect’, expectation of corporate tax reductions and reduction of financial industry regulation, and now the objective of dominating world energy markets. A strong U.S. economy would normally be positive for Canada, but the softwood lumber dispute and the upcoming NAFTA negotiations have raised questions about that link. Overlaid on these factors was the decline in oil prices in Q2.

How does all this affect the Canadian healthcare sector? The NASDAQ index is really a tech index, and tech profits are sometimes moved to biotech when the tech market gets frothy. The NASDAQ Biotechnology index is an indicator of the general health of big cap biotech companies, which are simply pharmaceutical companies with a different product mix. If this group is healthy, then Canadian small cap funds and retail investors have a neutral to slightly positive disposition to the Canadian sector. To date, U.S. big cap tech and biotech industries are healthy, which calms Canadian biotech investor nerves.

Canadian healthcare companies in the development stage generally rely upon institutional investors for funding, and retail investors for liquidity between deals. As such, the share price changes that I summarize and assess each quarter reflect retail trading, general sector sentiment, broad stock market trends and, most importantly from my perspective, corporate events and performance.

In the next post, I will assess the Q2 and H1 2017 share price performance of the Tier 1 Canadian healthcare companies.

[The author and his immediate family members may have long or short positions in the shares of some companies mentioned in or assessed during the preparation of this blog. Past share price performance may not be an indicator of future share price performance. This blog does not consider the investment objectives, financial situation or particular needs of any particular person. Investors should obtain professional advice based on their own individual circumstances before making an investment decision.]

As with all our posts, please see our full legal disclaimer