October 13, 2022

Q3 2022 Share Price Performance

Bouncing Along A Possible Bottom – Macro Factors Main Drivers of the Bumpy Ride

In this blog post, Bloom Burton’s equity research team summarizes the performance of the Canadian healthcare sector during 3Q-2022 and provides commentary on select stock movements and overall market trends.

Inclusion Criteria

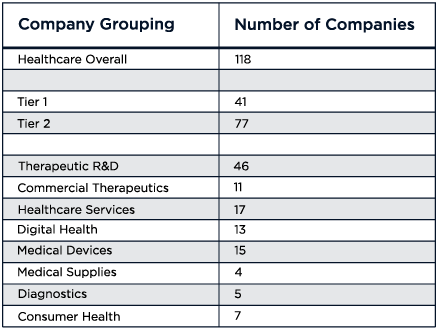

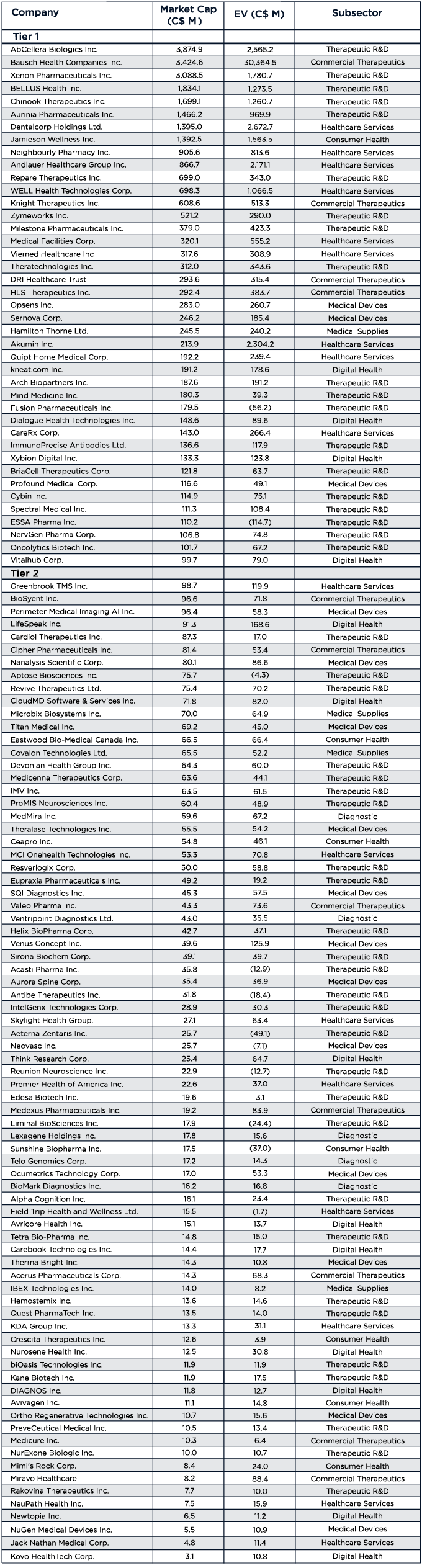

The analysis includes all Canadian publicly listed healthcare companies, defined as companies that are Canadian headquartered and/or listed on Canadian exchanges, with either a market cap (MC) or enterprise value (EV) of C$10M or greater at September 30. Our definition of healthcare includes companies operating in the following areas: therapeutic R&D; commercial therapeutics; healthcare services; digital health; medical devices; medical supplies; diagnostics; and consumer health. We do not include medical cannabis or psychedelic medicine companies (unless they are developing cannabis or psychedelic-based products under the traditional drug development regulatory process) or companies that operate long-term care facilities. Based on these criteria we identified 118 companies.

We classify companies as “Tier 1” and “Tier 2” based on their MC (previously based on EV) – Tier 1 companies are those with MC of >C$100M and Tier 2 are those with MC of <C$100M (for a complete listing of companies included in Tiers 1 and 2 of Bloom Burton’s “blog universe”, please see Appendix 1 at the end of the blog).

3Q-2022 Performance

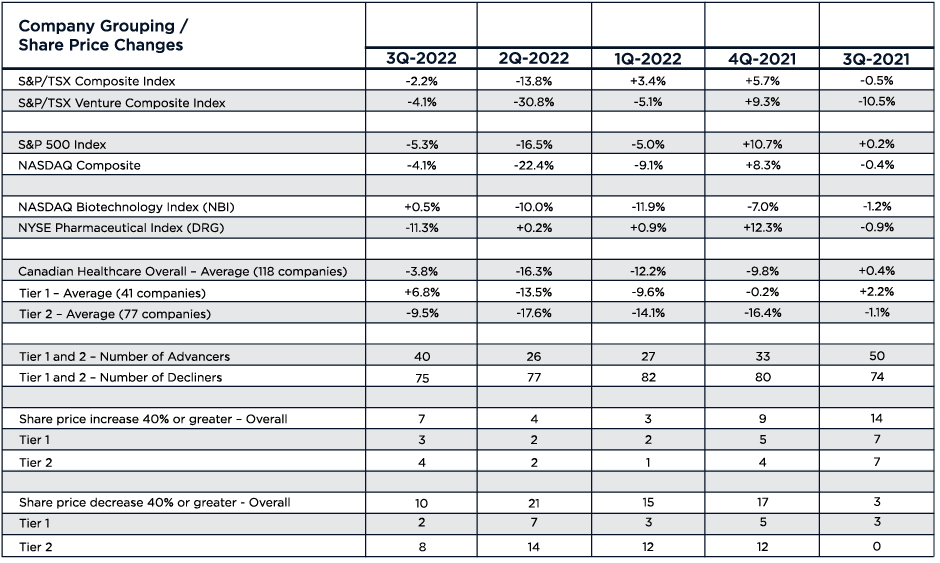

As a group, the 118 Canadian healthcare companies included in Bloom Burton’s 3Q-2022 blog universe were down an average 3.8% in the quarter, modestly underperforming the S&P/TSX Composite Index (-2.2%) and generally in line with the S&P/TSX Venture Composite Index (-4.1%).

In the U.S., biotech stocks rose slightly during 3Q-2022 – the NASDAQ Biotechnology Index (NBI) gained 0.5% in the quarter, outperforming the broader U.S. market (S&P 500 Index down 5.3%; NASDAQ Composite down 4.1%).

The tepid performance across all major indices has been driven by geopolitical tension which has contributed to both investor uncertainty and inflation (with energy prices spiking) along with COVID-related supply chain issues. That the NBI did comparatively well in 3Q-2022 is likely due to the sector’s dismal performance since 3Q-2021, with the index underperforming all other major indices – losing 30% from its high on August 30, 2021, heading into third quarter 2022. The underperformance over that period, in turn, can be blamed partly on the 70%+ positive move the sector made between March 2020, when COVID uncertainty was at its peak, and August 2021, when biopharma was loved – having “saved the world” with COVID treatments and vaccines. This was followed by a period of concern over drug pricing which culminated in the passing of The Inflation Reduction Act in August.

Despite factors weighing on biotech, the sector, as mentioned above, did modestly outperform the broader markets in the third quarter. This included beating pharma, with the NYSE Pharmaceutical Index (DRG) down 11.3% (vs the NBI’s 0.5% gain) – perhaps a sign that The Inflation Reduction Act’s drug pricing controls are expected to have a bigger impact on pharma companies. More likely, however, pharma had further to fall, with the DRG up 7% between August 2021 and July 2022 (vs the NBI’s 30% drop).

Among Canadian healthcare companies, larger Tier 1 companies, which are typically better capitalized and less risky, performed better than smaller Tier 2 companies in 3Q-2022 (+6.8% vs -9.5%, respectively).

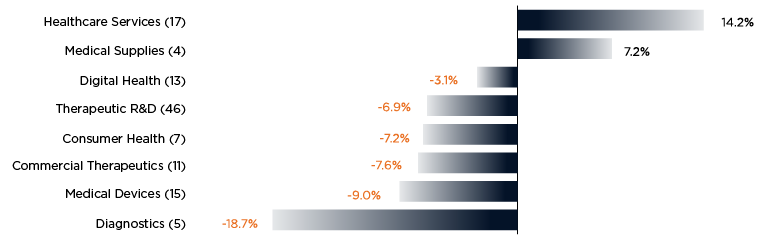

Among the healthcare subsectors in Bloom Burton’s Canadian tracking universe, the best performing subsectors were healthcare services (17 companies: +14.2%) and medical supplies (4 companies: +7.2%), which benefitted from the rebound in procedure volumes following COVID-19 restrictions. At the opposite end of the spectrum, the worst performing subsector was diagnostics (5 companies: -18.7%), with all other subsectors also posting negative returns, including digital health (13 companies: -3.1%), therapeutics R&D (46 companies: -6.9%), consumer health (7 companies: -7.2%), commercial therapeutics (11 companies: -7.6%), medical devices (15 companies: -9.0%) and diagnostics (5 companies: -18.7%).

3Q-2022 Healthcare Stock Performance By Subsector:

Tier 1 Company Performance

Overall, we included 41 companies in our Tier 1 analysis with MC of $100M or greater, which collectively had a 3Q-2022 return of 6.8%.

The number of Tier 1 advancers (21) just edged out the number of decliners (20) this quarter.

Notable Tier 1 advancers in the quarter were:

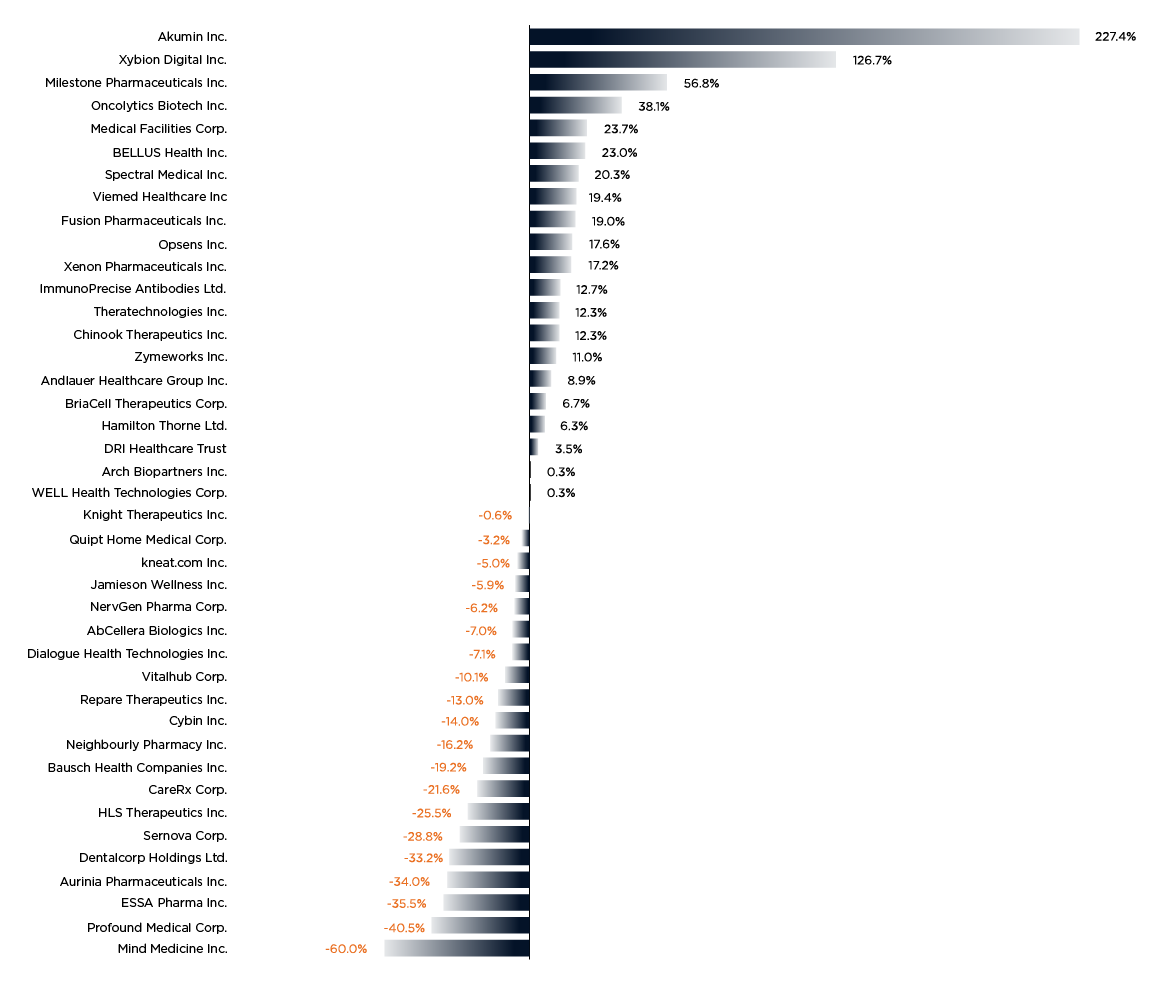

- Akumin Inc. – The stock gained 227.4% during 3Q-2022 (from all time lows early in the quarter), after the company provided a business update (including the sale of certain accounts receivables to a third party for US$30M) and announced a CFO transition, as well as completing a domestication to Delaware.

- Xybion Digital Inc. – The stock appreciated 126.7% in the quarter (also from an all time low reached in late June), after it announced its 4Q-2022 financial results, a US$12M credit facility and 1Q-2023 financial results.

- Milestone Pharmaceuticals Inc. – Not rebounding from an all time low (but a recent low in mid-May of this year), MIST stock appreciated 56.8% in 3Q-2022, continuing an upward trajectory that started in March 2020. During the quarter, Milestone reported 2Q-2022 financial results and provided a clinical update for its cardiovascular drug, etripamil, in phase 3 development for paroxysmal supraventricular tachycardia.

Notable Tier 1 decliners in the quarter were:

- Mind Medicine Inc. – The stock declined 60.0% during 3Q-2022, after the publication of a clinical trial by academic collaborators for MM-120 in general anxiety disorder and announced a US$30M public offering.

- Profound Medical Corp. – The stock depreciated 40.5% in the quarter, after the company announced 2Q-2022 financial results and provided a reimbursement update for TULSA-PRO, its tissue ablation device.

3Q-2022 Performance of Tier 1 Companies:

Tier 2 Company Performance

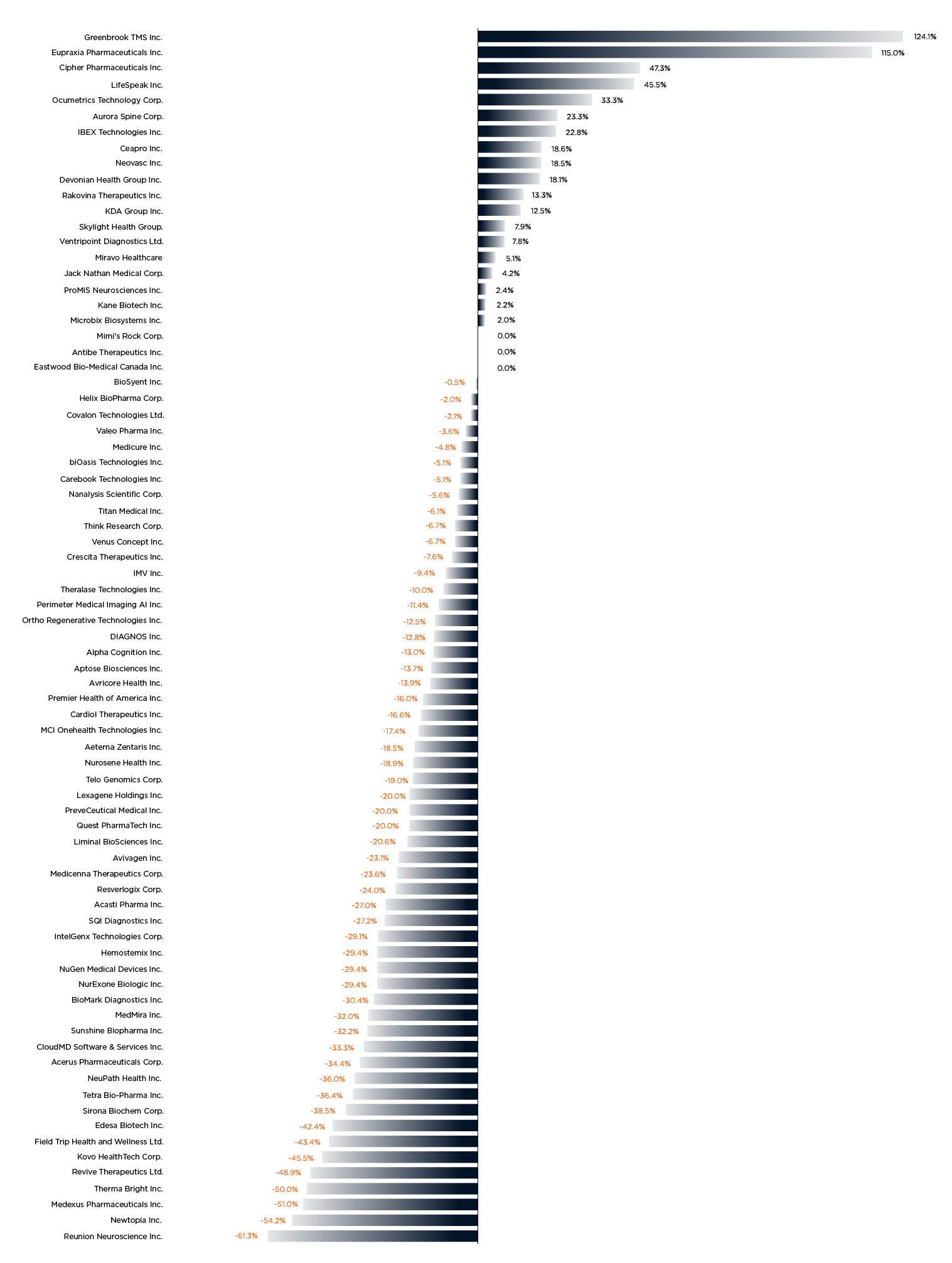

Overall, we included 77 companies in our Tier 2 analysis (with MC of less than $100M), which as a group had a 3Q-2022 return of -9.5%.

The number of advancers (19) was lower than the number of decliners (55).

Notable advancers in the quarter include:

- Greenbrook TMS Inc. – The stock was up 124.1% in the quarter, after the company announced the closing of an acquisition and a corresponding US$75M credit facility, as well as 2Q-2022 financial results.

- Eupraxia Pharmaceuticals Inc. – The stock appreciated 115.0% in 3Q-2022, after the company reported 2Q-2022 financial results and announced expansion of intellectual property for its pain drug, EP-104IAR.

- Cipher Pharmaceuticals Inc. – The stock climbed 47.3% after the company reported 2Q-2022 financial results, appointed a new CFO and announced a normal course issuer bid.

- Lifespeak Inc. – The stock rose 45.5% in the quarter (after declining 80.0% in 2Q-2022) corresponding to the reporting of 2Q-2022 financial results.

Notable decliners in the quarter include:

- Reunion Neuroscience Inc. – The stock declined 61.3% in the quarter, following its split from Field Trip Health and Wellness Ltd. (combined company formerly known as Field Trip Health Ltd.).

- Newtopia Inc. – The stock was down 54.2% in 3Q-2022, after the company announced a new engagement platform and brand refresh for chronic conditions and reported 2Q-2022 financial results.

- Medexus Pharmaceuticals Inc. – The stock lost 51.0% in the quarter, after the company provided an update on the treosulfan NDA submission.

- Therma Bright Inc. – The stock was down 50.0% in 3Q-2022, as the company awaited Emergency Use Authorization for its AcuVid COVID-19 Rapid Antigen Saliva Test.

- Revive Therapeutics Ltd. – The stock lost 48.9% in 3Q-2022, following an update on the phase 3 clinical trial for bucillamine in COVID-19.

- Kovo Healthtech Corp. – The stock declined 45.5% in the quarter, after the company reported 2Q-2022 financial results.

- Field Trip Health and Wellness Ltd. – The stock was down 43.4% in 3Q-2022, following its split from Reunion Neuroscience Inc. (combined company formerly known as Field Trip Health Ltd.).

- Edesa Biotech Inc. – The stock was down 42.4%, following the reporting of 3Q-2022 financial results and topline phase 2 data for EB05 in acute respiratory distress syndrome.

3Q-2022 Performance of Tier 2 Companies:

Appendix 1:

Disclaimer:

Information included in this blog post has been sourced from publicly available sources. No representation or warranty, express or implied, is made with respect to the accuracy, correctness or completeness of the information contained herein. The commentary in this blog post represents the views and opinions of Bloom Burton only and should not be relied upon as investment advice. Bloom Burton accepts no liability whatsoever for any direct or consequential loss arising from any use or reliance on the information contained herein. The blog is published on a quarterly basis.