January 19, 2015

The Tragedy in the Commercialization of Canadian Life Sciences Discoveries

“Australia excels in biomedical research but sucks at commercialisation.” Prof Frank Gannon, CEO & Director of QIMR Berghofer Medical Research

We may not be able to turn a phrase quite as elegantly as Dr. Gannon but what rings true for him, a leader in the drive for the commercialization of Australia’s life-sciences basic research, rings even more loudly in Canada. Gannon, the former Director General at the Science Foundation of Ireland, framed this statement at a symposium at which he was describing the prospective positive impact on commercialization of the recently-announced $20 billion Medical Research Future Fund just one year after the Canadian Government announced its $25 million Venture Capital Action Plan investment for the life-sciences in two Canadian venture capital funds.

The tragedy in Canada is twofold:

Firstly, this country has generated the most extraordinary portfolio of life-sciences resources in the world The paragraph, below, describes the raw materials that alone should have launched hundreds of companies of substantial economic and health-system benefit and, when one considers the remarkable output of universities ranging from Memorial to U. Vic, north to the Lakehead and the powerhouse that is the University of Alberta, the dearth of Canadian companies developing our highest–ranked biological discoveries is a costly tragedy of unconscionable magnitude.

Here is the paragraph from Canada’s Department of Foreign Affairs:

“Toronto has the largest faculty of medicine in North America, producing more peer-reviewed publications than any other medical centre in the world. Canada’s health sciences research community includes over 30,000 investigators in 16 medical schools and over 100 teaching hospitals and research Institutes”. http://www.tradecommissioner.gc.ca/eng/science/document.jsp?did=131981)

These papers, representing innovations and discoveries unparalleled by number in the world, are a national resource of excellence no less than Canada’s happy accident of having rocks, trees and pools of liquid and gaseous minerals that support the economic engines of our mining, forestry and oil-and-gas industries.

But the worst is yet to come!

Because, secondly, Canada has actively discouraged domestic investment in the commercialization of this very resource, its national resource of excellence, because makers of public policy simply have been blind to the magnitude of what it represents, evidentially unwilling to reverse an injudicious position that is contrary to Canada’s self-interest, or cowed by administrators unable to manage the complexity. This combination of nescience and adopted anxiety has resulted in lost opportunities for agriculture and patients and at enormous economic cost to provincial health systems(2) from the necessary importation of drugs from abroad. Such discouragement has not been present in our competitor to the south.

The tragedy is even more bitter in that no Canadian federal government for the past 35 years – the years during which biological exploration has been converted into value around the world – has understood the magnitude of the economic cost with which each one of them has burdened society by the deterrence to development of this national resource.

While provincial governments bear little of the blame for the perverse federal position there has been reticence in recognition by them of the immense magnitude of both economic and medical benefit that has been foregone and in which the provincial governments – both elected and bureaucratic – could have joined the campaign to undo the harm. Not one single federal government, irrespective of party, has come anywhere close to grasping the magnitude of its harm. In Ontario, the provincial government of Premier Bob Rae in 1994 enthusiastically received, with the intention of implementing most of the recommendations, a report from the Biotechnology Council of Ontario but, regrettably for Canada and the life-sciences industry, losing its mandate shortly after. In parallel, the tragedy has been compounded by the Toronto Stock Exchange’s de-emphasis of its role as crucial in creating an environment of vigorous encouragement to capital formation for small and medium-sized enterprises – understandable by virtue of that sector’s unimportance to the profitability of the public company it became post-demutualization. The last Premier of Ontario (to whom the TSX is responsible) who actively intervened, and who succeeded in his demand of the TSX that it creates and adopt specific policies and procedures and practices to foster and promote capital formation for SMEs, was Bill Davis, leaving office thirty years ago.

The presence in the current century of specific federal programs discouraging the investment in life-sciences together with the absence of specific programs for the encouragement of capital formation in public markets for SMEs have been the two greatest factors in the Canadian tragedy of the translation of its national resource of excellence. This nation has skills in science and finance that are the envy of the world and, in both regards in this matter, our talents are being buried meriting the biblical admonishment “….cast the worthless servant into the outer darkness. In that place there will be weeping and gnashing of teeth.”

This paper is not a solitary howl – nor even a recent one – but it is one that stubbornly continues unheard. One of Canada’s most eminent contemporaries, the architect of the Canadian Institutes of Health Research, formerly president of the Medical Research Council and founding chairman of Genome Canada, Dr. Henry Friesen, put it this way in a 2006 paper(1):

“Since Medicare came into being, Canada has invested over $1 trillion in support of the health care system, but has produced few if any brand name health products or services ………….. The Ontario Hospital Association in a 2003 study identified more than 240 major breakthrough developments originating in Ontario hospitals; yet few have yielded serious commercial success on a global scale. Why and how is this possible? It is not surprising because governments have not included economic outputs in the mandate of the health system. There is no expectation of and therefore no accountability for the economic dividends from the health system.”

In a 2002 paper(2) – but not even the earliest on the matter – Dr. Friesen again caught the bull’s-eye with this informed, but ignored(3), guidance to government:

“…..alignment of health and economic development policy is absolutely necessary to take full advantage of Canada’s existing strengths. We already have the world-class medical scientific talent, an outstanding international reputation for human health ingenuity, a strong and robust economy, an entrepreneurial business community, and an unwavering public commitment to a high quality health care system. Given those advantages, Canada’s health product trade deficit is paradoxical……….our health care system and our industrial health innovation sector can be an engine of economic growth that will contribute greatly to a sustainable health care system”.

But enough words – What are the data supporting this rant? Where is the evidence?

I refer again to the paragraph above – “Toronto has the largest faculty of medicine in North America, producing more peer-reviewed publications than any other medical centre in the world.”

And will add “Canada now captures only about 1% of that [US] market, even though we produce 3% of the world’s knowledge.”(3)

I submit that few would argue that this sadly-untapped resource should yield enough nuggets of substantial value on which to found enterprises translating those papers into human-health and agricultural products of value to those who would risk their capital for the development process. I further submit that none of the hundreds of companies that have successfully translated biological basic research into medicines have had access to any resource approaching the magnitude of that which lies at our feet.

So, given that we agree that either no, or exceptionally few, translational initiatives have been founded on a resource as deep as our own what have translational companies elsewhere been able to achieve with less? We will not burden the reader with lists of those products that have resulted from basic research but we will use, as a proxy, market capitalization which is a fair measure both of the success of the translations and of the economic prospects of those enterprises.

Firstly, we shall simply measure the economic value that life-sciences companies offer to a national economy and then we shall compare those to enterprises that exploit the rocks, trees and biogenic (abiogenc?) pools of Canada’s natural resources. Oh, and we shall throw in a bunch of banks and automotive companies just for fun.

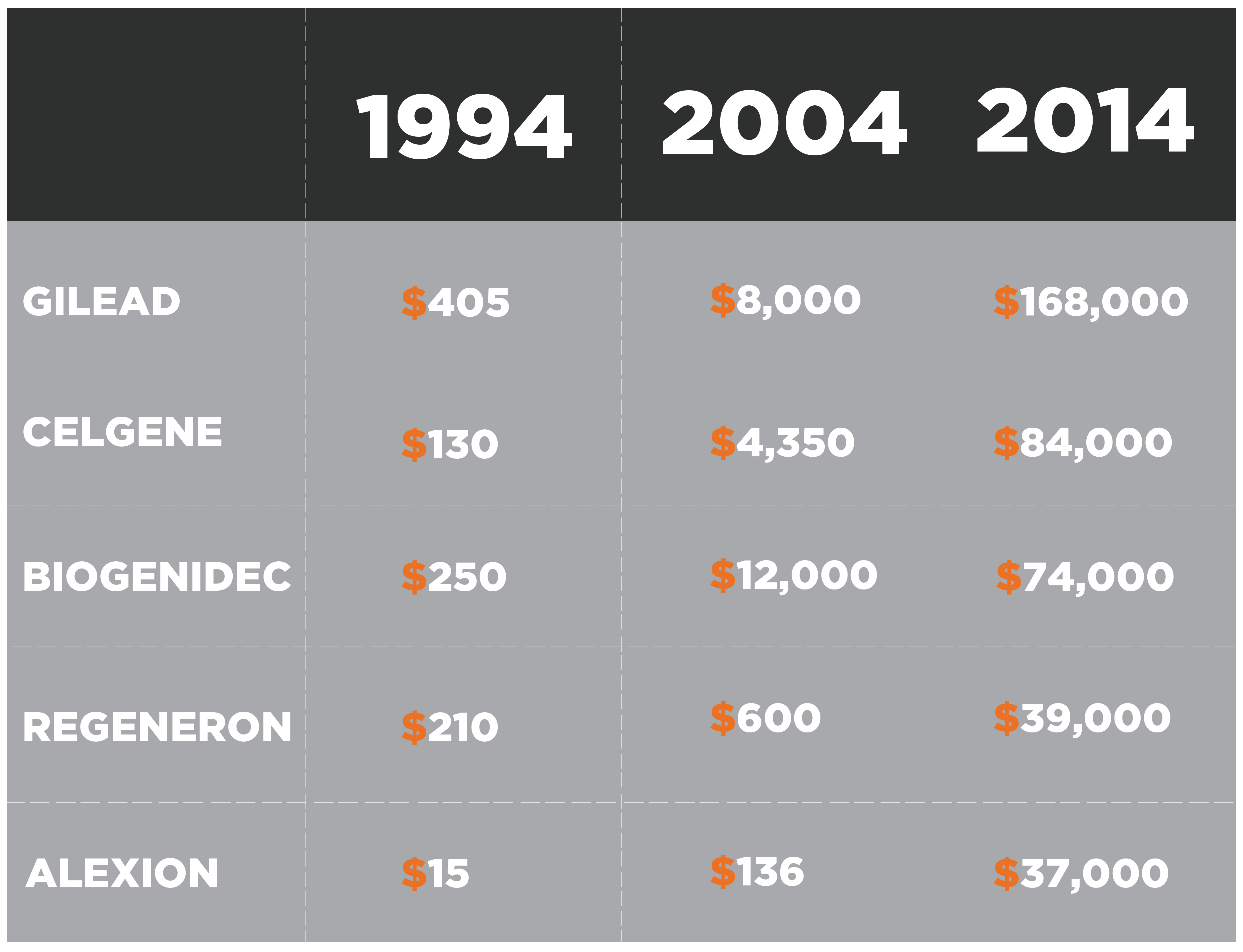

Over the past just 20 years five of today’s six largest translational companies accomplished this:

MARKET CAPITALIZATIONS – $000,000

Market Value in Millions

(valuations as at 12/2014)

So what?

Well, for a start, none of those are resident in Canada even though we boast, correctly, that we have “the largest faculty of medicine in North America, producing more peer-reviewed publications than any other medical centre in the world.”

However, everything is just fine because after all Canada’s competitive advantage doesn’t really live in all that exotic stuff but in rocks, trees and oil and gas – our free trade in automotive and in our world-class financial institutions .

Really?

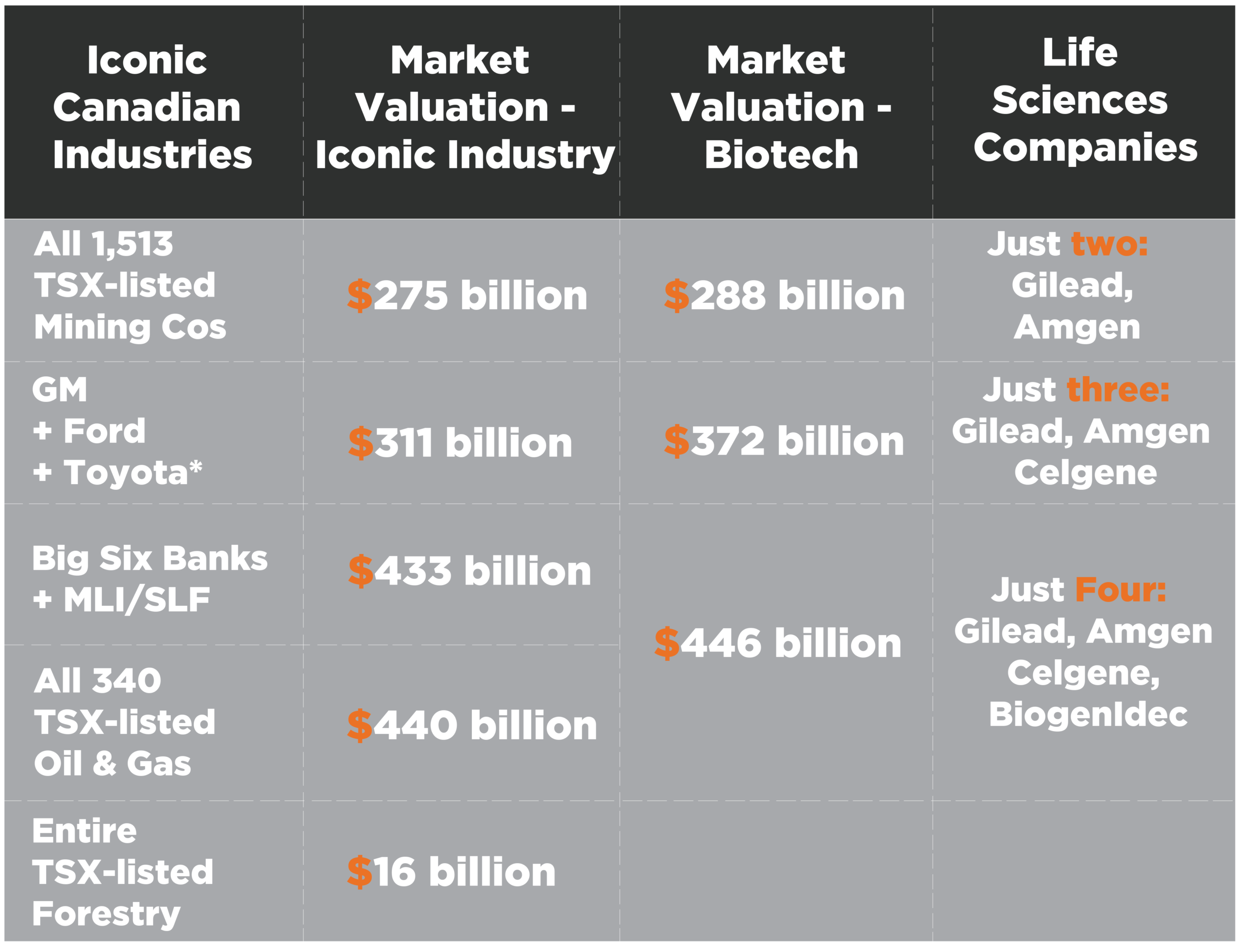

SECTOR MARKET CAPITALIZATIONS AS A PROXY FOR ECONOMIC CONTRIBUTION

(valuations as at 12/2014)

*Okay, so these are not Canadian but feature high in the minds of Canadian policymakers and in government subsidies. (Toyota, the largest automotive company in the world).

It is unconscionable that with our science-based resources that this table should exist.

So what is it that has specifically discouraged investment for the translation of basic research in the life-sciences into products useful in husbandry and human medicine? Well, surely, it must be that Canada is a country of wimps that have no appetite for the enormous risk that is required to develop biological resources. The hard evidence denies that out-of-hand since, for the past 50 years, highly-risk-tolerant Canadian investors have poured billions upon billions of dollars into natural resource exploration, development and, for as long as we were privileged to have the only speculatively-inclined exchange in the world, the Vancouver Stock Exchange, raw speculation. The process for this pouring is known as Flow-Through Shares(5) a device unique, to my knowledge, to Canada permitting investors to mitigate their risk by utilizing expenditures in exploration and development companies that were of no immediate tax benefit to the company and permitting those costs to reduce the net cost of the investment by ~50% or more, thereby reducing the risk.

Given that biological exploration and development is significantly more risky than geological the presence of the Flow-Through Share program is a specific disincentive to providers of capital to support biological exploration because that latter activity is more risky than, and the cost is ~twice that of, geological exploration. In geological exploration time-to-failure is short and in biological research can be extremely long – demonstrably as much as 15 years. In geological exploration a discovered asset has an international market price requiring only the ability to transport a mineral even in a raw state. In biological exploration neither the price nor the quantity has any certainty until well after the product is approved through a rigorous and expensive regulatory process. Any Canadian investor choosing biology over geology having a ~equal probability of exploration success would be barking mad. Add to this that our only national stock exchange, at least until the recent and welcome approval of the Aequitas Neo Exchange that has a stated commitment(6) to the encouragement of small-and-medium-sized enterprises, has, since its demutualization, had little presence of consequence in the encouragement of capital formation for SMEs then it is no wonder that the commercialization of Canada’s scientific excellence sucks.

The competitive advantage of nations does not lie in the ground it lies in the brain. It is expressed by enlightened government policies that, in respect of one of Canada’s most valuable assets, the evidence demonstrates, have been absent for the past 35 years. Notwithstanding this country’s having all the essential elements to be a world leader in husbandry and human medicine with its attendant economic benefit we are humiliated by just two ~25-year-old companies exceeding in value our entire 1,513 listed mining companies, just four exceeding in value all 340 listed oil and gas companies and those same four surpassing, in those few years, the value of the eight icons of Canadian banking and insurance that includes the almost-200-year-old Bank of Montréal.

Whichever elected federal government recognizes the magnitude of the folly of these 35 years of discouragement to development of our national resource of excellence will stand head and shoulders above its predecessors and whichever provincial government joins in recognizing the blatantly obvious economic impact on its constituency from the sector will bask not only in the recognition but will unleash a formidable economic engine. The solutions are straightforward, long overdue and require only vision and vigor.

(1) Enhancing Canadian Health and Wealth through Industrial Innovation. Innovation Health Review, March, 2006

(2) Dr. Henry Friesen, “New Models for Investing in Innovation in Health”, Discussion Paper, Public Policy Forum Roundtable, August 2002.

(3) Dr. Friesen is not alone. Of Benjamin Franklin it was said: “As always, his advice was good and, as was often also true, it was not followed.”

(4) Dr. Henry Friesen in his acceptance speech for Life Sciences Ontario – Life Achievement Award, February 22, 2005

(5) Canada Revenue Agency – Flow-through shares (FTSs) Certain corporations in the mining, oil and gas, and renewable energy and energy conservation sectors may issue FTSs to help finance their exploration and project development activities. Junior resource corporations often have difficulty raising capital to finance their exploration and development activities. Moreover, many are in a non-taxable position and do not need to deduct their resource expenses. The FTS mechanism allows the issuer corporation to transfer the resource expenses to the investor. A junior resource corporation, in particular, benefits greatly from FTS financing.

http://www.cra-arc.gc.ca/tx/bsnss/tpcs/fts-paa/menu-eng.html

(6) Aequitas Innovations Inc: June 25 ’13. Executive Summary of the Position Paper – “ A Capital Formation Process in Tune with Issuers and Investors”

As with all our posts, please see our legal disclaimer.