April 17, 2014

Building a Biotech Company in Canada

Building a biotech company in Canada has always been a challenge. IP laws that lag behind the US and Western Europe, a major exchange that is usually five to ten years behind on implementing new regulatory regimes, and access to capital and human resources are constant themes, replayed over and over, year after year.

I have been involved with biotech in this country for 33 years now, the last 20 as a publicly traded company CEO. It has been a frustrating experience knowing how simple it would be to deal with these issues, and put us on at least an equal footing with our largely US cousins in the industry. The last two, in particular, could be addressed by the federal government today.

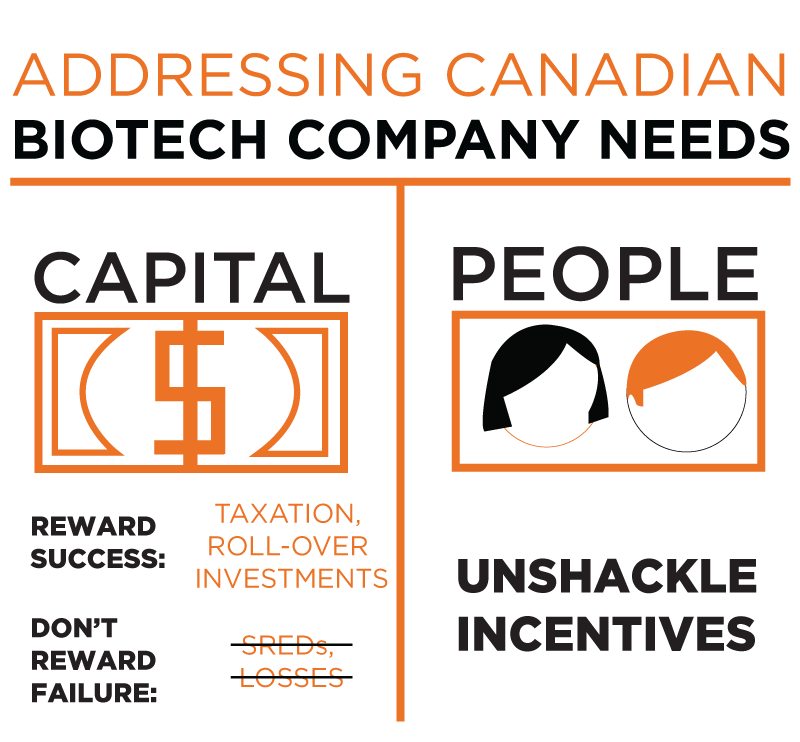

Access to capital is critical. At Oncolytics, we have spent a relatively small amount, $250M to date, in the development of our lead product. Our industry chews through more than $30B a year, virtually all of it raised through private capital. Governments do not (and should not) support this effort, spending their tax revenueses on programs with unacceptable risk profiles. Most products fail along the way. So how to increase capital flows without government subsidies? We have a vigorous investment climate in Canada; money is available. A standard comment internationally is that Canadians either invest in high-risk ventures (oil and gas, mining, other resources) or low risk ones (our banks). How do we get this existing tendency to invest in higher risk ventures translated to investment in biotech? And by extension any knowledge based R&D based business? What has been demonstrated to work elsewhere is to allow the risks and the rewards of investment both fall on the investor. So on the risk side: no tax loss carry forwards, no SREDs. Rewarding failure does not incentivize investment. On the reward side: the same tax rate of 25% of maximum income tax rates for capital gains, dividend, and interest income, with no minimum hold periods and no penalty for making your living as an investor. If the investment is rolled over into a new investment within 12 months, then the tax rate falls to 0%. As we spend most of our money on people, and they pay income taxes, tax revenues actually increase using this regime.

Access to people is also critical, and is currently limited by our ability to compensate colleagues competitively. A critical tool, stock options, is under assault from both a company and personal perspective. The successful movement to classify options as an expense has reduced our ability as companies to use them as a recruiting and retention tool, and is frankly nonsensical. Options are not an expense. They are dilutive to earnings/share and financial statements should reflect earnings/basic shares and earnings/fully diluted shares. On the personal side, taxes should be paid on options when the underlying shares are sold. Paying taxes on them when they are exercised discourages people from investing in their own companies. And even more destructive is a movement to mark taxation on the increase in value of unexercised options. The net effect of all of this is that options are becoming useless as a tool. And we end up having to spend more cash, which disadvantages our current shareholders.

I wish we could spend an afternoon (one, that’s all it would take!) to fix all of this. But in the meantime we will continue to shift our industry to the US, and file our patents there, list on an exchange there, hire people there, and raise capital there. And of course get our products approved there first. After all, why would we want to treat Canadians with products that were invented here?

[Editor’s note: Brad Thompson is CEO of Oncolytics Biotech®, whose website can be found here]

As with all posts on this blog, please see the full legal disclaimer.