February 13, 2015

Looking Inside the Biotech Black Box (Part 3)

More complicated – and useful – mathematics

In Part 2 of this blog series, we looked at some basic investment mathematics – the time value of money, NPV and the risk-free cost of capital. However, nothing in biotech is risk-free and the risks associated with biotech can be large and numerous.

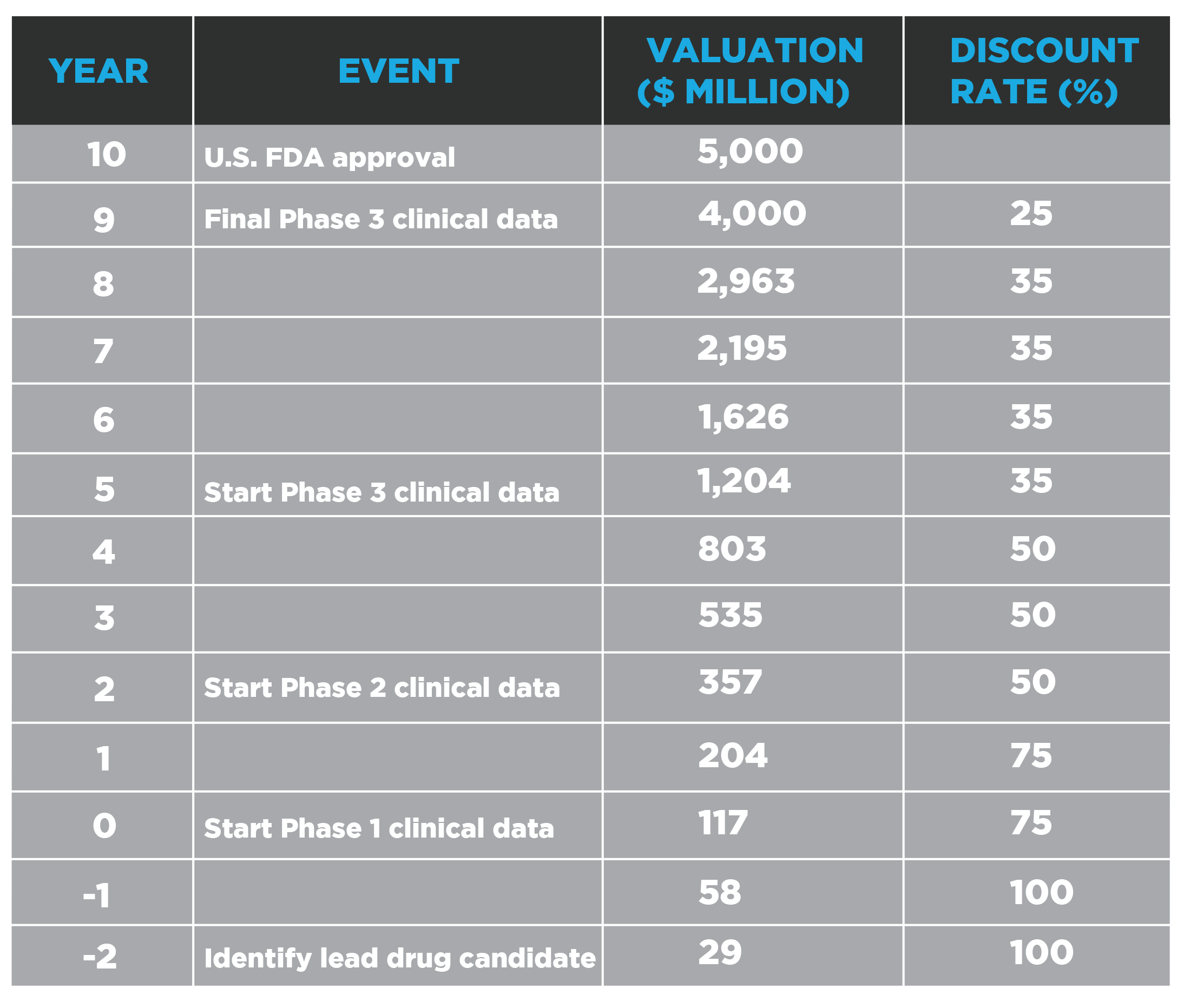

In this blog, I am going to start with the assumption that a product receiving U.S. FDA approval has a value of $5 billion, based on a discounted cash flow or other financial analysis. If this product is just starting the first Phase 1 study, it is probably about 10 years from approval – the time can vary widely depending upon the product type and clinical indication. How do we work backwards from that valuation at approval to the valuation at various times during the development process?

- Step 1: outline the path to regulatory approval and the critical events along that pathway – completion of clinical trials with positive clinical data

- Step 2: choose discount rates which reflect the risk associated with that stage of product development

- Step 3: apply the discount rates using the formula

Valuation (year Y) = Valuation (year Y+1) X (100 / (100 + discount rate))

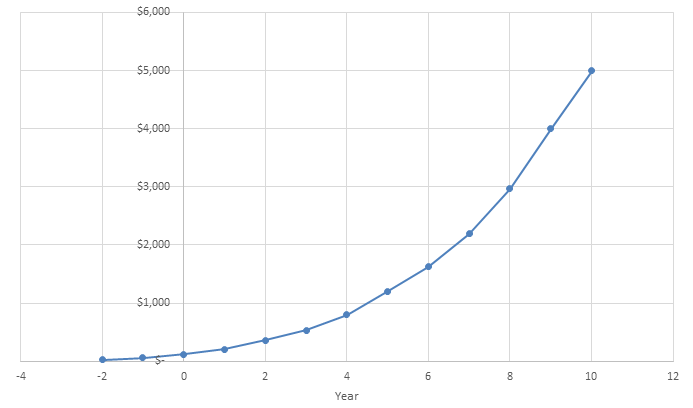

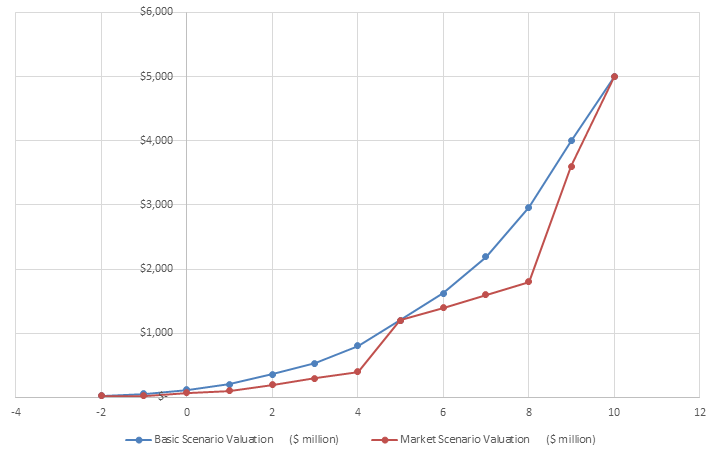

The result is illustrated in the following table and graph.

Valuation ($Millions)

Remember that this is simply a mathematical model and there are many factors which must be considered in order to make the valuation curve more realistic. The mathematical model is useful for showing how valuation will trend upward on positive clinical data but it is not very useful for establishing valuation at a specific point in time.

- Many factors could impact the original assumption of a $5 billion valuation upon FDA approval, including competitors reaching the market first, clinical data not being competitive or superior or, on the positive side, the selling price is higher than expected.

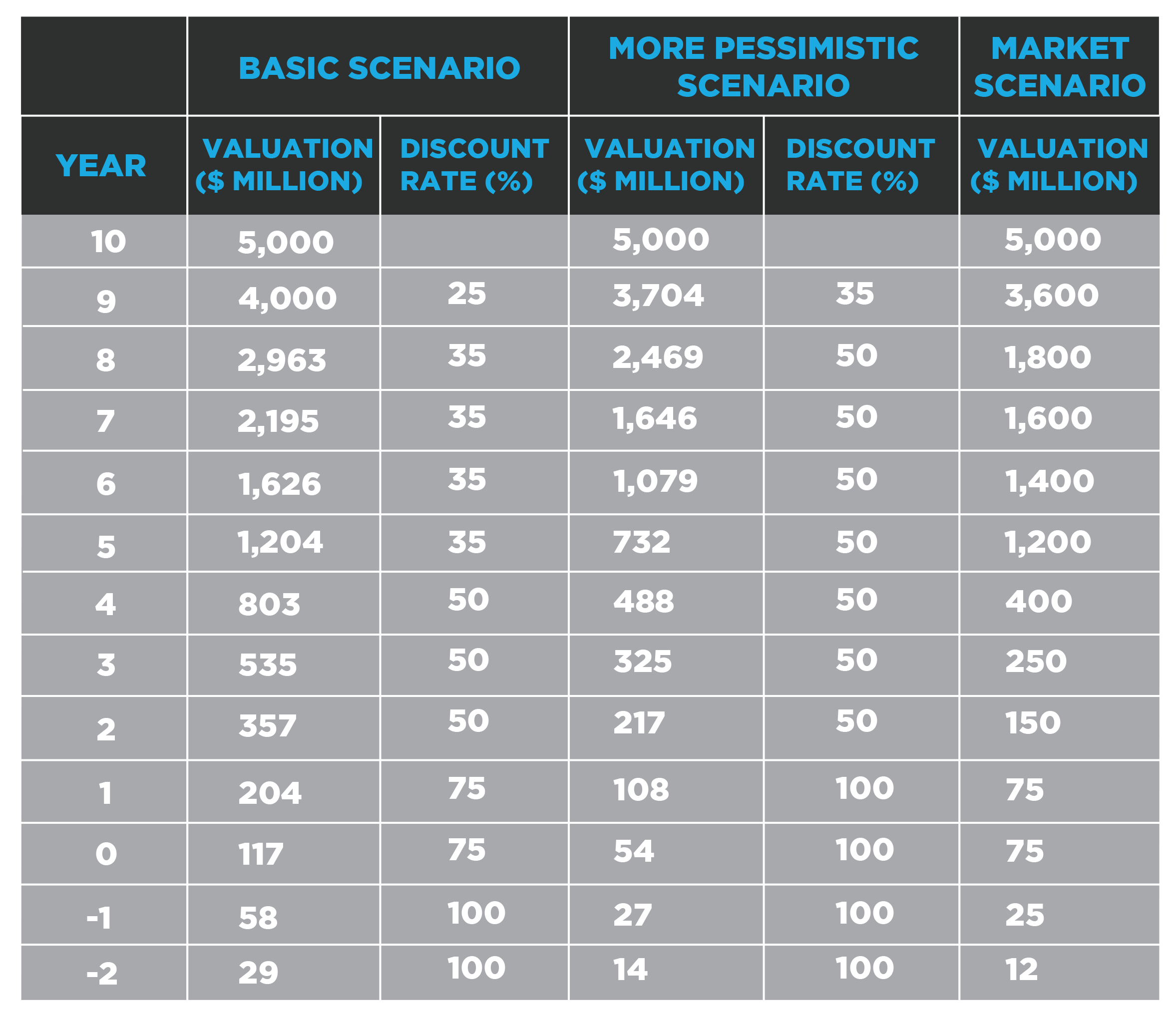

- The discount rates are educated guesses, chosen based on my 20+ years of experience developing valuation models. There is no book or article dictating a discount rate of 38% for a Phase 3 colorectal cancer product or a discount rate of 150% for preclinical and Phase 1 development of a technology that has not been validated. The impact of increases in the discount rates are shown in the More Pessimistic Scenario in the table below.

- The assumption that value grows continuously during product development is not realistic since the market generally only gives full credit for the growth when there is a positive outcome at the end of a specific stage of development. Valuation could be impacted by extraordinary success of a related compound in the same clinical indication. Valuation also depends on many factors that are unrelated to this specific product, such as positive or negative momentum, movement of the biotech and a broader stock market. The impact of the market’s need for data before recognizing the increased valuation is shown in the Market Scenario in the table and graph below.

Market vs. Basic Scenario

It is impossible to calculate an absolute valuation for a product during its preclinical and clinical development. Using one or a combination of discounted NPV analysis, assessment of comparable companies or any other valuation methodologies, the best conclusion that can be reached is that a valuation is reasonable.

There is a continuous need to understand and balance the risks and potential rewards. In the next few parts of this series, we will continue looking at valuation of the potential rewards before we move on to looking at the risk side of the equation.

[The author and his immediate family members may have long or short positions in the shares of some companies mentioned in or assessed during the preparation of this blog. Past share price performance may not be an indicator of future share price performance. This blog does not consider the investment objectives, financial situation or particular needs of any particular person. Investors should obtain professional advice based on their own individual circumstances before making an investment decision.]

As with all our posts, please see our full legal disclaimer.