February 1, 2016

Q4 and Annual 2015 Share Price Performance (Part 3)

In this blog, I am going to comment on the Q4 and 2015 annual performance of the Tier 2 group of 49 companies with share prices of between $0.10 and $0.99 to start 2015. IMRIS (taken private after a Chapter 11 filing), Premier Diagnostic Health Services (which no longer has a healthcare focus) and Medworxx Solutions (acquired) were excluded from this analysis.

Q4 2015 Tier 2 Performance

- Decliners significantly outnumbered advancers by 31 to 18

- Average and median share price changes were -11% and -6%, respectively

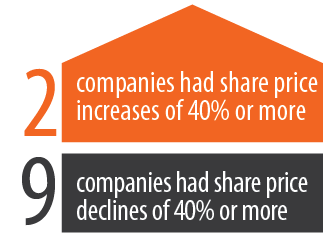

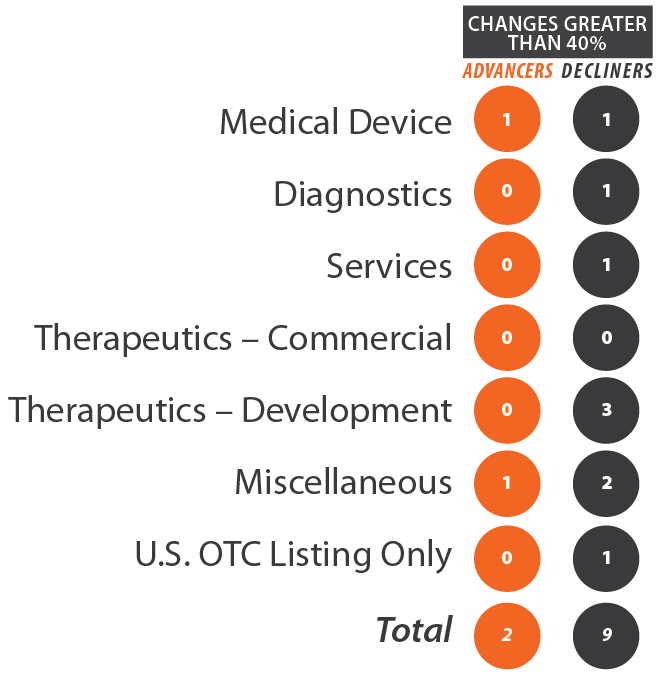

- Only two companies had a share price increase of 40% or more

- Ceapro (+63%) – announced improved financial results

- Theralase Technologies (+48%) – announced FDA marketing authorization for a next generation medical laser system

- Nine companies had share price declines of more than 40%

- Agility Health (-41%) – there were no significant announcements

- Annidis Health Systems (-41%) – continuing losses, perhaps financial concerns and very low trading volumes

- GLG LifeTech (-43%) – biggest decline correlates with a large volume trade on Dec. 18

- Aeterna Zentaris (-46%) – possibly related to the share consolidation and financing

- Acerus (-55%) – continuation of the Q3 decline

- Miraculins (-67%) – the biggest drop correlates with the announcement of a strategic review

- Vivione Biosciences (-67%) – bouncing along a bottom with almost no trading volume

- Advanced Proteome Therapeutics (-68%) – largest drop correlates with announcement of a discrepancy in animal data between two labs

- Axxess Pharma (-91%) – continuation of a year long decline

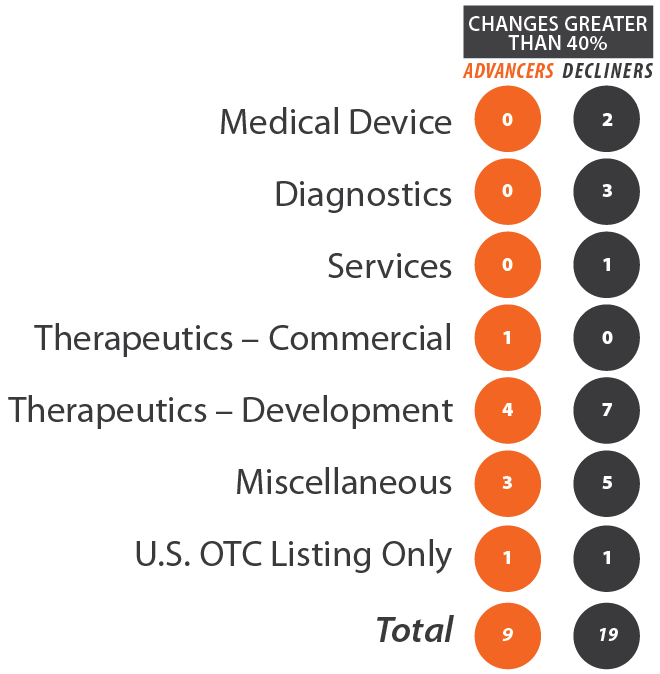

Annual 2015 Tier 2 Performance

- Decliners more than doubled advancers by 33 to 16

- Average and median share price changes were -3% and -29%, respectively

- Nine companies had share price increases of 40% or more (+50% to +428%) and nineteen companies had share price decreases of 40% or more (-44% to -99%)

- The best performer in this group in 2015 was Theratechnologies (+489%), whose performance masks the real performance of the sector. If the Theratechnologies data is excluded, the average share price decline changes from -3% to -12%. If the second best performer is also excluded, the average drops even further to -17%.

2014/2015 and Other Comparisons

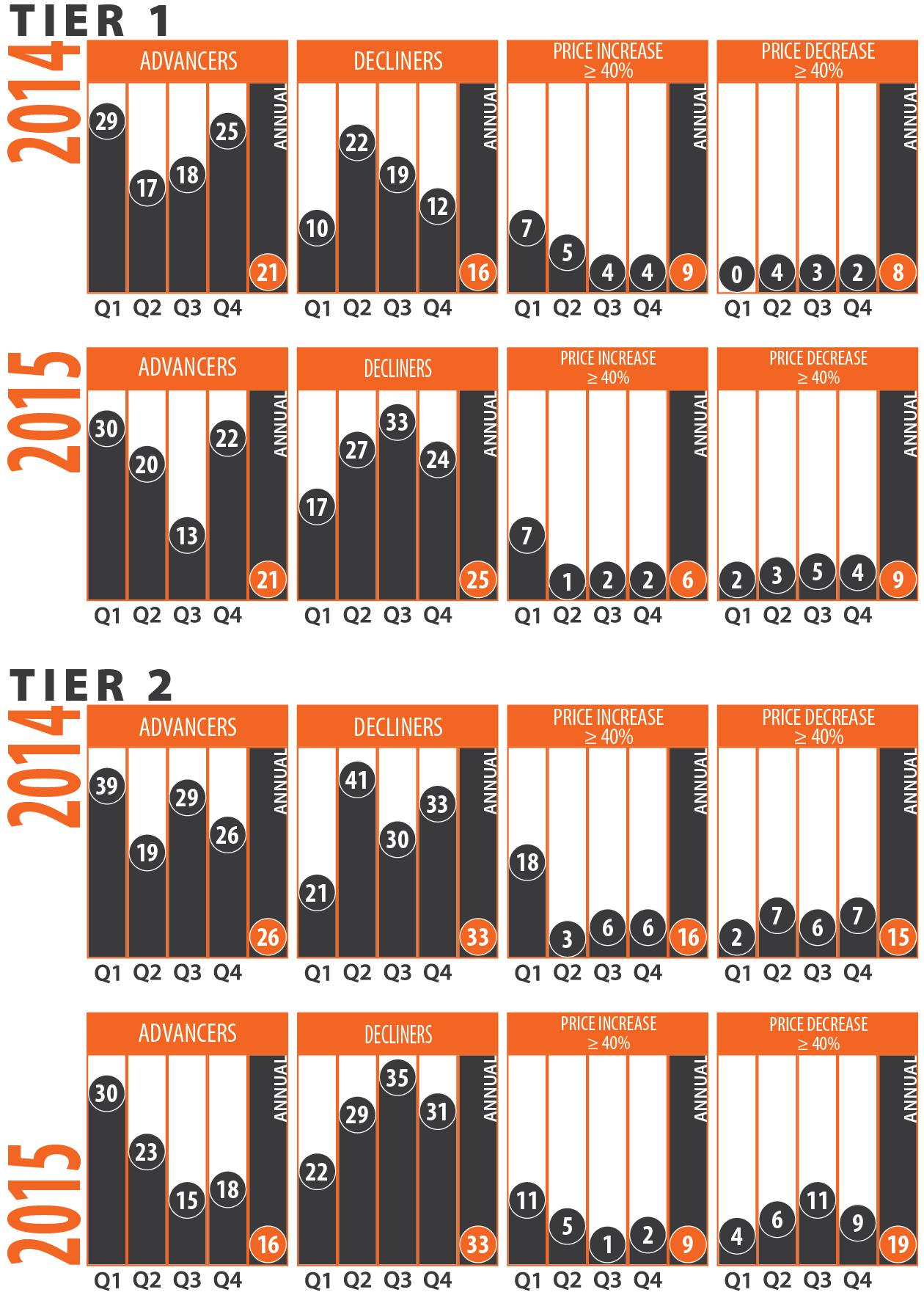

Tier 1 vs. Tier 2: this comparison is essentially small and mid-cap vs. micro cap, which is the main reason there is less volatility in the Tier 1 group as indicated by the number of companies with price changes greater than 40%.

Quarterly comparisons: Q1 appears to have been the quarter of optimism, although this will probably not hold true in 2016. There does not appear to be any year to year pattern in the other quarters. Performance in individual quarters may be impacted more by macro events.

2015 vs. 2014: On average, performance in 2015 was worse than in 2014 for both the Tier 1 and Tier 2 groups. I think the major factor was events in Q3 2015 – decline in global markets, rapid negative market reaction to drug pricing concerns and the broad negative performance of the micro and small cap companies listed on the TSX Venture Exchange.

Medical Marijuana Group

Medical marijuana companies listed on the TSX Venture Exchange and OTCBB were monitored for share price performance in 2015. Many of these companies have been public for less than 12 months, have low trading volumes, are in the early stages of commercialization and are not yet profitable.

-

- While there were 8 decliners and no advancers in Q3, Q4 was positively impacted by the election of a Liberal federal government favoring the legalization of marijuana. In Q4, there were 5 advancers and 2 decliners with average and median share price changes of +73% and +29%, respectively.

- For 2015, there were 4 advancers and 3 decliners with average and median share price changes of +9% and +11%, respectively.

- Looking to 2016, sector movement will probably be linked to possible legislative changes.

Looking Ahead

-

- The NASDAQ Biotech Index peaked on July 20, slowly declined along with major stock markets and then plunged 20% between September 17th and 29th, triggered by the intensely negative response to the news on Turing Pharmaceuticals drug price increase for Daraprim. This index did recover some of that drop and the biotech sector looked forward to the usual boost from the J.P. Morgan healthcare conference in the second week of January. Instead, this index had declined 16% by the end of this conference as investors reduced their exposure to risky sectors.

- The Looking Ahead section of my Q3 blog commented on market volatility and included the following sentence – ‘This is not normal for big caps and major indices, which scares retail investors and further reduces their risk appetite.’ This sentence aptly applies to the chaotic decline of global stock markets during the first two weeks of 2016. Until the global markets stabilize, the risk appetite of institutional and retail investors is unpredictable.

[The author and his immediate family members may have long or short positions in the shares of some companies mentioned in or assessed during the preparation of this blog. Past share price performance may not be an indicator of future share price performance. This blog does not consider the investment objectives, financial situation or particular needs of any particular person. Investors should obtain professional advice based on their own individual circumstances before making an investment decision.]

As with all our posts, please see our full legal disclaimer.